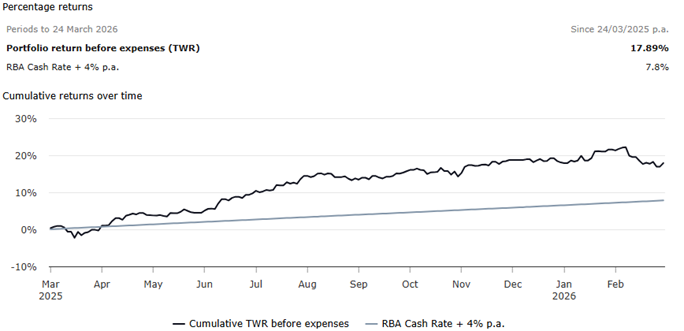

The Active Income Strategy continues to do what it’s designed to do, deliver high, consistent income with capital growth over time, while cushioning volatility when markets get tougher – as they are currently.

Performance remains solid. Over the past 12 months, the portfolio has returned 17.9% to yesterdays close, materially ahead of the RBA Cash Rate +4% benchmark (+7.8%), adding +10.1% of value over that period. Since inception in July 2017 (to end of Feb), the strategy has delivered +10.51% p.a., outperforming the benchmark by ~5% p.a., with cumulative value add of +80.43%.

That’s exactly what this portfolio is built for – steady compounding through a mix of yield, franking, and selective capital growth. When markets are weak, some investors become more uncomfortable than others, but however you feel about the current state of play, it’s worthwhile for investors to assess whether we’re invested in the right strategy for our risk tolerance. As we sit this morning, the ASX 200 is off 9% from the top. The Active Income Portfolio is not immune, but it does historically perform better than the market in weakness, and this pullback is no different, experiencing a portfolio drawdown of less than 4%.

chart

12-month performance of the Income Strategy (source: Praemium)

chart

12-month performance of the Income Strategy (source: Praemium)

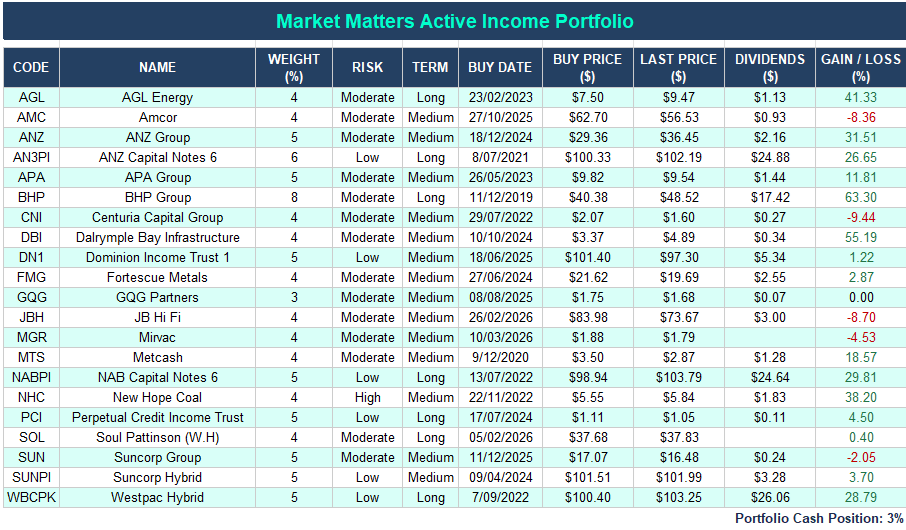

Positioning of the portfolio is first and foremost about income, but that does not come at the expense of total return. The strategy invests across high yield equities and a selection of debt securities.

- High-yield equities (banks, resources, infrastructure)

- Hybrids / income securities (AN3PI, NABPI, SUNPI, WBCPK)

- Credit exposure (PCI, DN1)

- Defensive industrials & REITs (APA, MGR, CNI)

A few themes are driving performance across the portfolio:

Resources are still delivering income given commodity prices overall remain strong, even after the recent correction. This is particularly true for Iron Ore, Copper & Coal – areas where the portfolio is exposed. Positions like BHP and New Hope (NHC) continue to underpin yield, albeit with more cyclicality. NHC in particular highlights the trade-off – weaker earnings recently, but still strong cash flow and rising dividends over time.

- Infrastructure & real assets are holding up. Names like Dalrymple Bay Infrastructure (DBI) and APA Group (APA) continue to provide stable income streams with some inflation linkage

- Banks & hybrids are doing their job. Core exposures to ANZ and hybrid securities are benefiting from higher rates, supporting income while maintaining relatively low volatility.

But not everything is working. Rate-sensitive exposures are under pressure. REITs like Mirvac (MGR) and asset managers like GQG have struggled, partially on the back of higher interest rates. Consumer exposures such as JB Hi-Fi (JBH) and Metcash (MTS) reflect a more cautious consumer backdrop.

More recently, Credit / listed income vehicles have been mixed, with holdings like DN1 and PCI now trading below NTA, although we still believe they offer stable income, now at attractive levels.

From here, we see the best opportunity into areas that have been impacted by rising bond yields / interest rates. The playbook is fairly simple. Higher Oil prices are feeding inflationary fears, pushing up bond yields. We believe that as/when positive developments take place around the Middle East conflict, oil prices will fall, bringing bond yields with it. Lower bond yields will provide a catalyst for property and retail-related stocks (and fixed-rate corporate bonds for that matter), and these are the areas we see best risk/reward at current levels.

- Ultimately, the Income Portfolio isn’t about shooting the lights out; it’s about consistency, lower volatility, and high levels of tax-effective income.