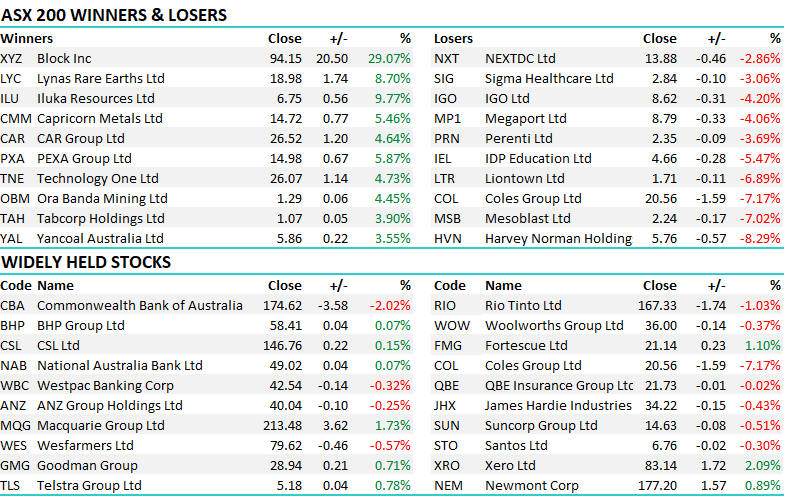

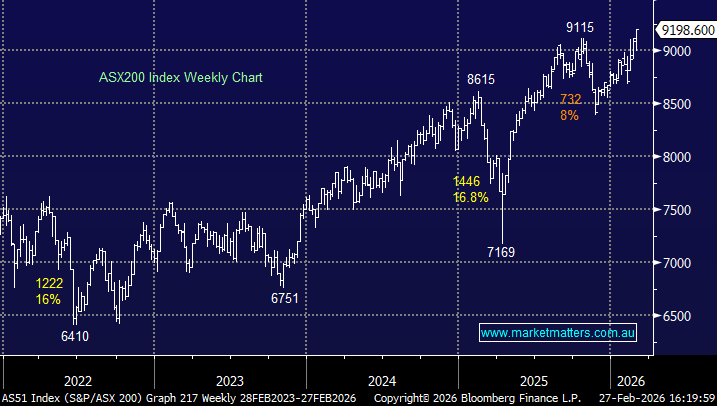

The ASX 200 posted another all-time high on Thursday, closing up +0.5% after flirting with the psychological 9200 level in the morning. IT stocks led gains, with the sector surging +5.2% amid a broad-based rally that saw 7 of 11 sectors trade higher. Health care rebounded 1.6% following recent weakness, supported by a strong interim result from Ramsay Health Care. The miners again provided meaningful support, rising 1.0% and pushing to fresh highs as BHP extended its record run, trading above $58 for the first time - even after closing 50c below its intra-day high Australia’s biggest stock added more than 20 points to the index, or more than 40% of the day's gain.

The ASX 200 powered to a fresh all-time high on Wednesday, ending the session with triple-digit gains. In character with recent action on the stock/sector level, gains weren’t as broad-based as we would usually expect for such a barnstorming day, with more than 30% of the main board closing lower, along with the consumer services, defensive utilities and consumer discretionary sectors. It's starting to sound like a stuck record, but the miners performed the heavy lifting with BHP Group (BHP) contributing ~28% towards the day's gain - the “Big Australian” is on fire, adding another +3.2%, extending its surge so far in 2026 to +24%, and we’re less than two months in!

The ASX200 closed flat on Tuesday despite less than 40% of the main board advancing. The story at the stock/sector level remained the same, with miners and banks offsetting losses across the broader market. BHP, Westpac and NAB added 24 points to the index. BHP, often referred to as the Big Australian, made new all-time highs on Tuesday, trading above $55 for the first time while it reported strongly this month, its starting to remind us of the feeding frenzy where ETF and momentum buyers drove CBA towards $200 in the first half of 2025:

The ASX200 wobbled on Monday, as was largely expected, following Trump's tariff tantrum over the weekend, which created uncertainty around US trade policy. The local bourse slipped 0.6%, with over 70% of the main board retreating, but another strong session from the miners stemmed the losses, with heavyweight BHP again posting a fresh all-time high, closing up +19% year-to-date.

On Friday, the US Supreme Court struck down most of Trump’s sweeping tariff policy under the International Emergency Economic Powers Act, ruling in a 6-3 vote that the law does not authorise the president to impose tariffs. Markets reacted positively to the ruling, with stocks rising, including Amazon, up more than 2%, alongside gains in retailers Home Depot and Five Below, amid hopes of relief from tariff-driven cost pressures and sticky inflation.

The ASX 200 posted a new intra-day high on Thursday before slipping into the close, ending a strong day up 79 points, or 0.9%. As reporting season gathers pace, yesterday’s session delivered another round of outsized moves from companies both beating and missing expectations.

The ASX 200 rallied for a 3rd consecutive day on Wednesday, closing back above the psychological 9000 level courtesy of a 4% rally by NAB following another solid earnings update from a “Big Four” bank.

The ASX200 surrendered much of its early gains on Tuesday but still ended the day up 0.2%. We almost felt like a one-stock index at times yesterday with BHP at one stage popping above $54, up more than 7%, for the first time. Even with the “Big Australian” closing back under $53, up +4.7% on the day, it still added 40-points to the ASX200, basically double its net gain on the day

Monday saw the ASX200 experience a choppy day, which came as no surprise, with Chinese markets closed for the Lunar New Year and the US closed overnight for Presidents Day - it’s the year of the horse in China, which has a bullish feel to it, being associated with energy, independence and drive.

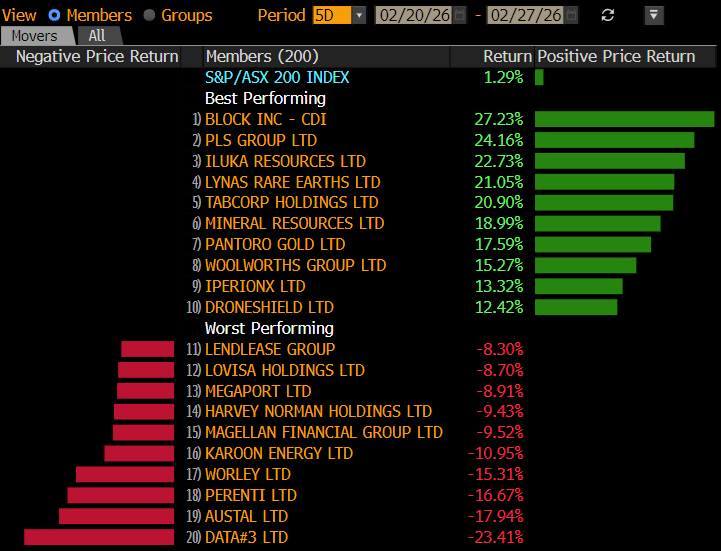

AI is increasingly impacting stocks and financial markets as a whole. Recent weeks have seen capitulation-style selling wash through some sectors, with investors fearing AI disruption is rewriting business models.

The ASX 200 powered to a fresh all-time high on Wednesday, ending the session with triple-digit gains. In character with recent action on the stock/sector level, gains weren’t as broad-based as we would usually expect for such a barnstorming day, with more than 30% of the main board closing lower, along with the consumer services, defensive utilities and consumer discretionary sectors. It's starting to sound like a stuck record, but the miners performed the heavy lifting with BHP Group (BHP) contributing ~28% towards the day's gain - the “Big Australian” is on fire, adding another +3.2%, extending its surge so far in 2026 to +24%, and we’re less than two months in!

The ASX200 closed flat on Tuesday despite less than 40% of the main board advancing. The story at the stock/sector level remained the same, with miners and banks offsetting losses across the broader market. BHP, Westpac and NAB added 24 points to the index. BHP, often referred to as the Big Australian, made new all-time highs on Tuesday, trading above $55 for the first time while it reported strongly this month, its starting to remind us of the feeding frenzy where ETF and momentum buyers drove CBA towards $200 in the first half of 2025:

The ASX200 wobbled on Monday, as was largely expected, following Trump's tariff tantrum over the weekend, which created uncertainty around US trade policy. The local bourse slipped 0.6%, with over 70% of the main board retreating, but another strong session from the miners stemmed the losses, with heavyweight BHP again posting a fresh all-time high, closing up +19% year-to-date.

On Friday, the US Supreme Court struck down most of Trump’s sweeping tariff policy under the International Emergency Economic Powers Act, ruling in a 6-3 vote that the law does not authorise the president to impose tariffs. Markets reacted positively to the ruling, with stocks rising, including Amazon, up more than 2%, alongside gains in retailers Home Depot and Five Below, amid hopes of relief from tariff-driven cost pressures and sticky inflation.

The ASX 200 posted a new intra-day high on Thursday before slipping into the close, ending a strong day up 79 points, or 0.9%. As reporting season gathers pace, yesterday’s session delivered another round of outsized moves from companies both beating and missing expectations.

The ASX 200 rallied for a 3rd consecutive day on Wednesday, closing back above the psychological 9000 level courtesy of a 4% rally by NAB following another solid earnings update from a “Big Four” bank.

The ASX200 surrendered much of its early gains on Tuesday but still ended the day up 0.2%. We almost felt like a one-stock index at times yesterday with BHP at one stage popping above $54, up more than 7%, for the first time. Even with the “Big Australian” closing back under $53, up +4.7% on the day, it still added 40-points to the ASX200, basically double its net gain on the day

Monday saw the ASX200 experience a choppy day, which came as no surprise, with Chinese markets closed for the Lunar New Year and the US closed overnight for Presidents Day - it’s the year of the horse in China, which has a bullish feel to it, being associated with energy, independence and drive.

AI is increasingly impacting stocks and financial markets as a whole. Recent weeks have seen capitulation-style selling wash through some sectors, with investors fearing AI disruption is rewriting business models.

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

Verication email sent.

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

!

Invalid One Time Password

Please check you entered the correct info, please also note there is a 10minute time limit on the One Time Passcode

To reset your password, enter your email address

A link to create a new password will be sent to the email address you have registered to your account.

Market Matters members receive daily market reports, real-time trade alerts, full access to 5 portfolios and dynamic company data.

Choose how you'd like to proceed:

We have a range of membership options to suit your needs and budget, why not join today and get unlimited access to the premium Market Matters service.