Portfolio Construction and Aus vs US equities

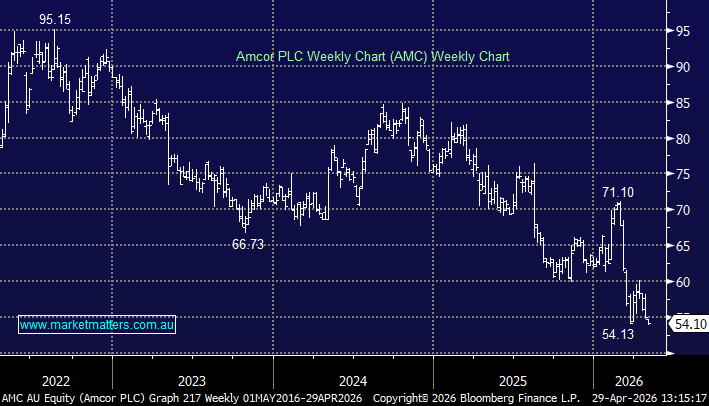

To The MM team, Great work guys, keep up the amazing content. Not looking for personal advice more a matter of strategy and philosophy. You run multiple portfolios across different themes (Growth, Income, Small Cap and International). Us mere mortals have our equities bundled into a single portfolio where we cherry pick ideas from different styles. So my question, with the forecast US returns (and Tech in particular) likely to outpace the ASX, how would you deal with underperforming Aussie shares. In particular: AMC and MGR. No doubt they will recover, but with a 12-18 month horizon it seems to me it could be better to cut and run then redeploy the cash into a hedged US ETF's. Any comments would be appreciated. Charles