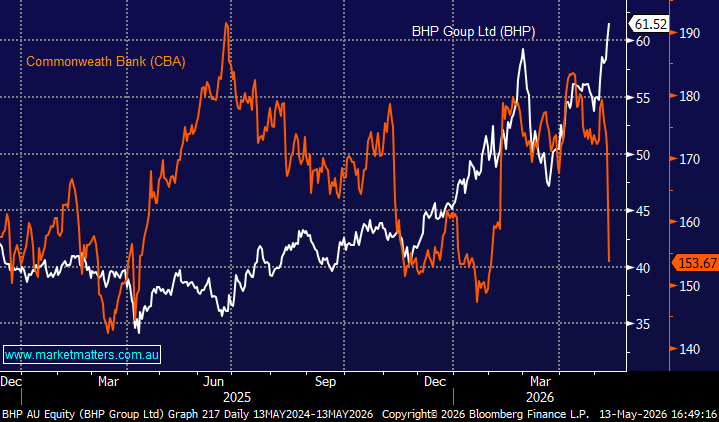

While CBA captured the news yesterday for all the wrong reasons, BHP again made new all-time highs, trading above $62 for the first time as copper continued to rally. As a sidenote, the game of musical chairs between BHP and CBA continued on Wednesday, with the “Big Australian” as BHP was referred to on the old trading floors reclaimed top spot as the ASX’s largest company after a session which saw a more than 13% difference in performance.

BHP Group (ASX: BHP): is estimated to yield 3.5% ff in the next 12-months and as the largest copper producer in the world, its perfectly positioned for what MM believes is the start of the commodities Supercycle, which is already underway, with Cu front and centre as global electrification gathers momentum. – MM owns BHP in our Active Growth Portfolio and Active Income Portfolio.

Commonwealth Bank (ASX: CBA): is estimated to yield 3.3% ff in the next 12-months with Australia’s largest bank the purest play on Australian housing and household credit, which in the past has been one reason it often commands a premium valuation—but also why it is most sensitive to property market weakness and consumer stress. We agree with the market’s re-rating of CBA yesterday, and it remains expensive in our opinion.

At MM, we continue to prefer ANZ Group (ASX: ANZ) and Westpac (ASX: WBC) for banking exposure, although we remain significantly underweight the sector in both our Active Growth Portfolio and Active Income Portfolio. To pre-empt member questions, we can see CBA testing the $140 area and BHP $70 through 2026/7 implying the elastic band has further to stretch.

- We believe the banks, and in particular CBA, will underperform the ASX through 2026.

MM believes BHP will outperform CBA and the banks over the next year

Add To Hit List

chart

BHP Group (BHP) v Commonwealth Bank (CBA)

chart

BHP Group (BHP) v Commonwealth Bank (CBA)