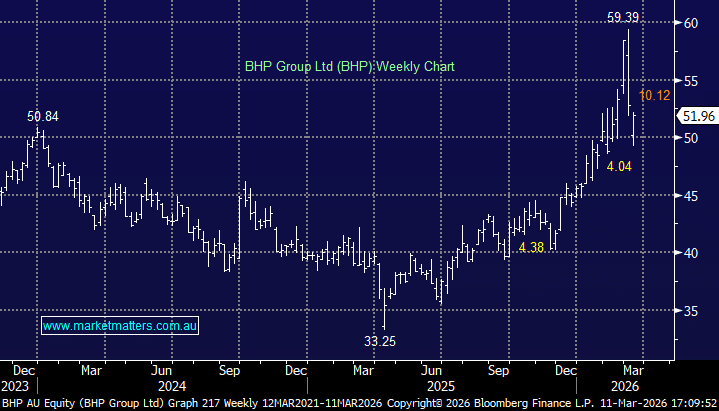

BHP has already corrected 17% from last week’s high, although it has paid a $1.03 fully franked dividend along the way. The firm iron price is supportive of this diversified miner, but it’s now more of a copper play, and the lasting impacts of the Iran War could weigh on the industrial metal in the coming weeks/months. A high oil price is a headwind for global growth, which is directly correlated to copper – we are considering increasing our copper exposure if we see another leg lower in the sector, but it’s unlikely we will add to our already sizeable position in the “Big Australian.” Alternative copper stocks to increase our exposure to the industrial metal include upweighting Sandfire (SFR) or buying Capstone Copper (CSC), or the gold/copper play Evolution Mining (EVN).

- We are looking for some consolidation by BHP between $50 and $59 – MM owns BHP in its Active Growth Portfolio and Active Income Portfolio.

MM is long and bullish BHP

Add To Hit List