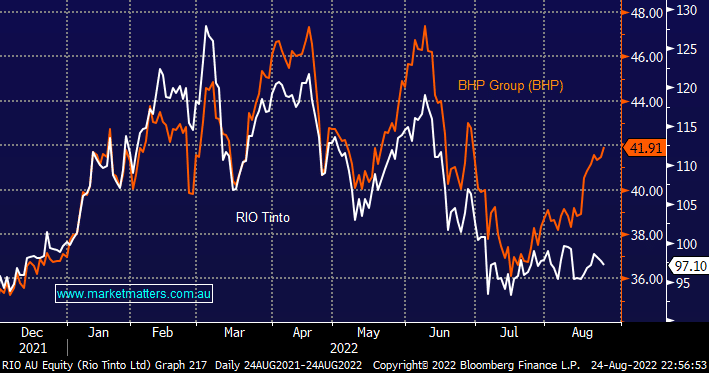

The last couple of months have seen a huge and uncharacteristic divergence between BHP and old rival RIO i.e. RIO has underperformed the index only bouncing +5.6% from its June low whereas BHP has advanced over +17%, more than 3x its rival. We like BHP’s corporate moves over the last 12-months where its spun off its oil assets into Woodside Energy (WDS) and bid for copper miner OZ Minerals (OZL) very clear steps to a more ESG future and although iron ore and coal still dominate its current earnings the company has clearly flagged its intention for the future.

- We believe BHP’s high ASX index weight since its reunification of listing structures has had a hand in this divergence.

- However, we see no reason to buy RIO over BHP until it takes more discernible steps to commence its evolution from its primarily iron ore business model.

- We are long BHP looking forward to its $US1.75 fully franked dividend in September but we can see ourselves reducing our large position slightly as the iron ore picture clouds due to huge economic headwinds building in China.

MM continues to prefer BHP over RIO

Add To Hit List