BHP delivered a solid 1H FY26 result in February, with revenue and underlying profit broadly in line with expectations, while beating on the dividend. Operationally, production across iron ore and copper rose modestly, but the key highlight was the earnings mix, with copper now contributing 51% of group earnings. Guidance was also upgraded at key copper assets, reinforcing the improving momentum in this growth division.

- BHP has transformed itself over the last decade to a copper-led miner with iron ore playing a secondary role and potash set to deliver a greater contribution in the next decade.

The company also struck an opportune $US4.3bn silver streaming deal with Wheaton, monetising a byproduct while retaining core exposure and balance sheet strength – a well-timed move with silver very” hot” at the time. While near-term analyst valuations may be weighed down by softer iron ore forecasts, BHP’s increasing leverage to copper and strong execution across its portfolio continue to underpin confidence in future cash flows.

- BHP remains a quality iron ore miner, but it’s likely to dance more of a copper jig in the coming years.

In our opinion, BHP is a world-class miner offering excellent exposure to copper and iron ore, both of which are underappreciated at current levels. The Big Australian is forecast to yield ~4.7% fully franked, making it an attractive buy/hold.

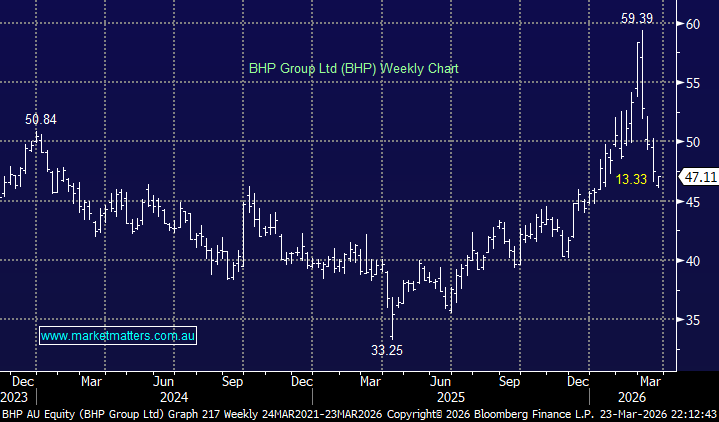

- We can see BHP making new highs as the copper price recovers – MM owns BHP in its Active Growth Portfolio and Active Income Portfolio.

MM is long and bullish toward BHP around $47

Add To Hit List