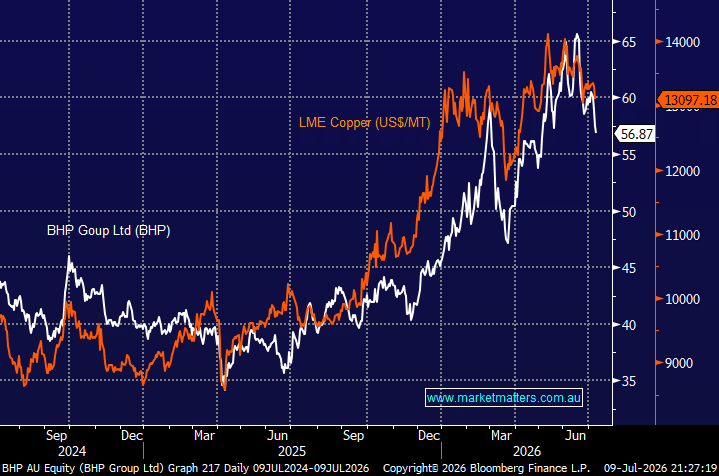

The correlation between BHP and Spot LME Copper over the last 2-years is 0.91, a very high positive correlation, reflecting BHP’s significant copper exposure and the market’s tendency to price the stock as a copper proxy. BHP’s copper assets, including Escondida (the world’s largest copper mine) and Olympic Dam, make it one of the most copper-leveraged large-cap miners globally. And as BHP continues to grow its copper revenue, this correlation is likely to remain elevated or even strengthen over time.

As an interesting comparison, BHP’s old main revenue source, iron ore, now has just a 0.12 correlation to the stock, essentially negligible, compared to copper (0.91) over the same period. Ironically, even though Sandfire has a far higher percentage of its revenue coming from copper, its correlation to the industrial metal is only 0.95. The big difference is that BHP is increasing its copper contribution while Sandfire’s (SFR) copper earnings dominance is set to ease. While copper generated 74% of SFR’s FY25 revenue, forecasts suggest this will moderate to 55–61% over FY26–28 as silver becomes a more meaningful contributor, supported by the ramp-up of SFR’s polymetallic MATSA operations in Spain.

Hence, while we hold SFR for its copper exposure, BHP is our preferred copper play into FY27, and if and when we do decide to trim our Cu exposure, it may well be through SFR.

- We like the risk/reward towards BHP after its 15% correction following union issues in Port Headland and a 12% pullback in copper prices.

MM is long and bullish towards BHP around $57

Add To Hit List

chart

BHP Group (ASX: BHP) v LME Copper ($US/MT)

chart

BHP Group (ASX: BHP) v LME Copper ($US/MT)