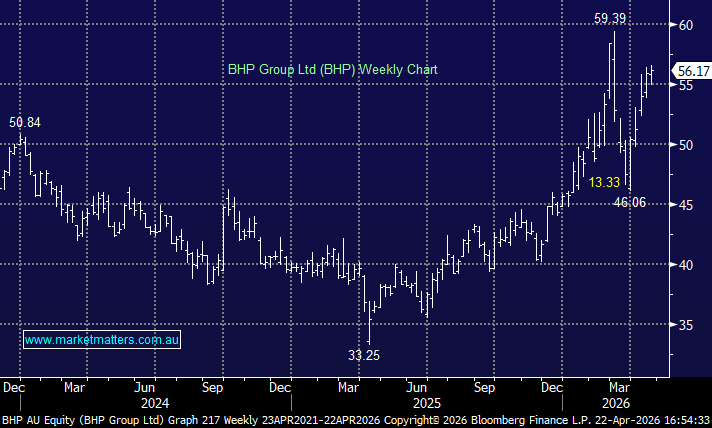

BHP +1.2%: traded higher after a solid March quarter from an operational perspective, while they also came to terms with China’s state-backed buyer, China Mineral Resources Group for the sale of Iron Ore – something that had been hanging over the stock.

BHP’s WA iron ore output came in at 69.8Mt for the quarter on a 100% basis, ahead of market expectations, while management kept FY26 iron ore guidance unchanged at 251–262Mt.

The China agreement was important. Iron ore remains BHP’s cash engine, and a clean trading relationship with its biggest customer base is fundamental to earnings certainty. The dispute had dragged on for months and had started to bite, particularly around Jimblebar, where quarterly output nearly halved sequentially to 10.9Mt as restrictions on certain BHP ore types disrupted normal trade flows.

- Overall, Iron ore was solid, copper was a touch softer in the quarter at 476.8kt, but management still expects full-year copper production to land in the upper half of guidance.

They also struck a positive tone around costs. Mike Henry said the group’s centralised procurement capability and low-cost operations have positioned it well against rising energy and consumables costs stemming from the Middle East conflict.action

MM remains long and bullish BHP

Add To Hit List