BHP delivered a solid 1H FY26 result in February, with revenue and underlying profit broadly in line with expectations, while the dividend surprised to the upside. Operationally, production across iron ore and copper edged higher, but the standout was the evolving earnings mix, with copper now contributing ~51% of group earnings. Guidance upgrades across key copper assets further reinforced momentum in what is increasingly becoming the company’s primary growth engine, even though it failed to acquire Anglo American (LN:AAL) last year.

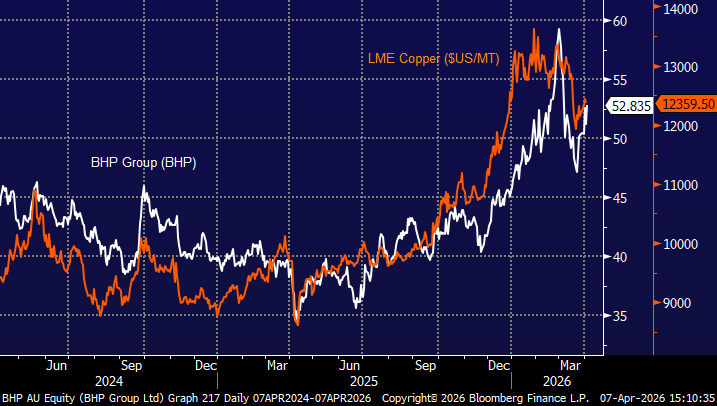

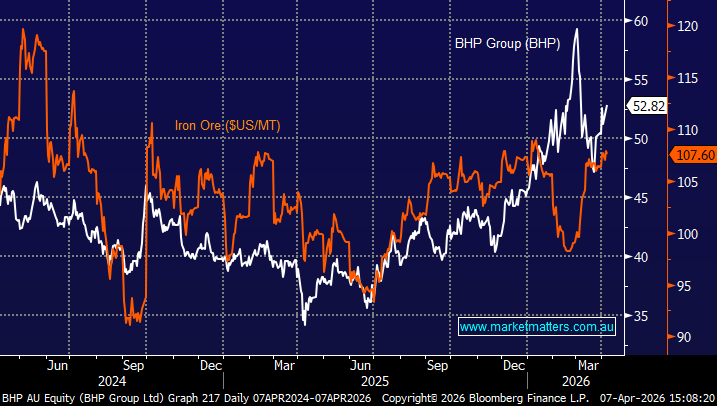

- BHP has tracked the iron ore price at times over recent years. But didn’t drive its move towards $60 through February, into early March.

Over the past decade, BHP has reshaped itself into a copper-led miner, with iron ore still a high-quality earnings pillar and potash emerging as a longer-term contributor. Recent capital management, including the $US4.3bn silver streaming deal with Wheaton, highlights disciplined execution—monetising by-products while maintaining balance sheet strength. While softer iron ore expectations may weigh on near-term valuations, if we’re correct it could help in the 2H. BHP’s growing leverage to copper and strong portfolio execution underpins our confidence in future cash flows, with the stock well positioned to benefit as copper prices recover from their -20% war related sell-off.

- We are bullish towards BHP through 2026 looking for a retest of $60, plus a ~$1.15 full franked dividend in August – we own BHP in our Active Growth and Income Portfolios.

When we look at BHP against the copper price over the same timeframe its clear that BHP is now being driven by the industrial metal as opposed to the bulk commodity, i.e. BHP is now a copper stock with an important contribution from iron ore. Taking into account our view toward iron ore through 2026, and core positive outlook towards copper, we believe BHP will continue to deliver for our two respective portfolios. Note we prefer BHP over Mineral Resources (MIN) for debt and balance sheet reasons, but the latter’s lithium exposure make it an increasingly appealing stock to sit alongside BHP in a portfolio as an iron ore play adding diversified tailwinds from other key metals.

- We continue to prefer BHP over RIO from a growth perspective due to its commodities mix, or skew toward copper.

MM is bullish towards BHP in the $53 area

Add To Hit List