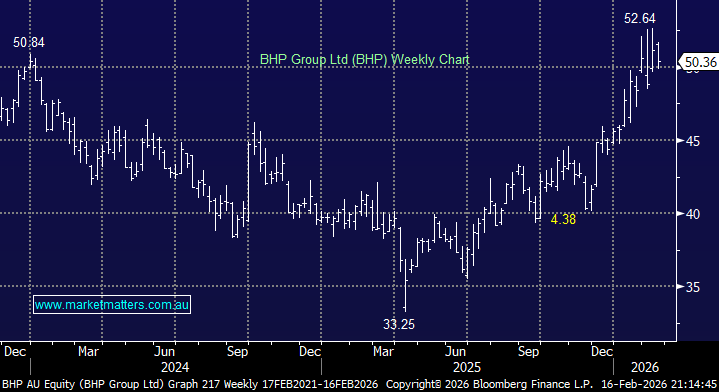

BHP delivered a solid result, with headline profit inline with expectations, as BHP continues to demonstrate operational resilience with improving momentum in copper.

- Revenue US$27.9bn vs US$26.88bn estimate

- Underlying profit US$6.20bn v US$6.25bn estimate

- Dividend US73c vs US65.3c estimate

Operationally, iron ore and copper production were up a modest ~2% YoY, though the earnings picture is what really jumped out with copper now contributing 51% of 1H FY26 group EBITDA. FY26 copper guidance was increased at Escondida and Antamina, and reaffirmed at Spence.

BHP also announced a long-term silver streaming agreement with Wheaton Precious Metals, receiving US$4.3bn upfront tied to its share of silver production at Antamina in Peru as well as a 20% trail on silver delivered moving forward . The deal monetises silver as a byproduct while retaining full exposure to the core copper-zinc asset and is not expected to increase reported debt.

BHP delivered a lift in the dividend, underscoring the resilience of the balance sheet and confidence in future cash flows. Near-term sentiment may take a hit given iron ore weakness, however the business continues to execute strongly at its copper projects at just the right time.

- MM owns BHP in its Active Growth Portfolio and Active Income Portfolio.

MM is long and bullish towards BHP

Add To Hit List