BHP won’t enjoy any impact from potash on its revenue until 2026 at the earliest, but it will, over time, create a more environmentally friendly company as its earnings profile evolves, i.e. FY23 48% iron ore, 31% copper and 21% coal. The further expansion by BHP into potash was flagged/expected, but it reminded us that we like the direction this flagship Australian miner is heading.

BHP believes the potash demand could double by 2050, taking it to ~$US50bn as the global population is set to rise towards 10 billion and food demand will increase by around 50%, making more efficient farming essential for quality of life – the megatrend. If these numbers prove correct, potash should substantially improve BHP’s earnings and diversification away from more traditional commodities.

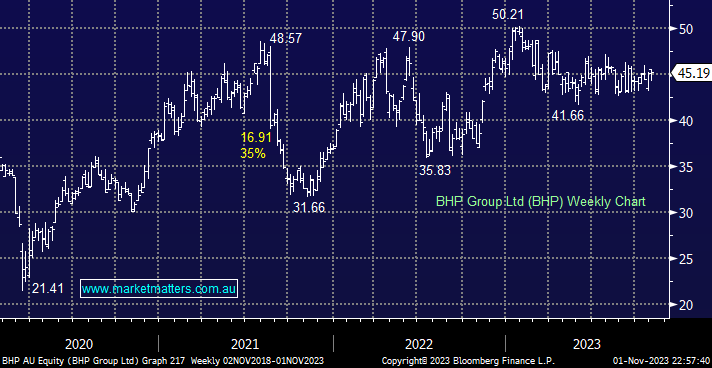

- No change, we are likely to trim our BHP holding around $50 and increase under $40 – if it’s not broken, don’t fix it!

MM is long and bullish toward BHP

Add To Hit List