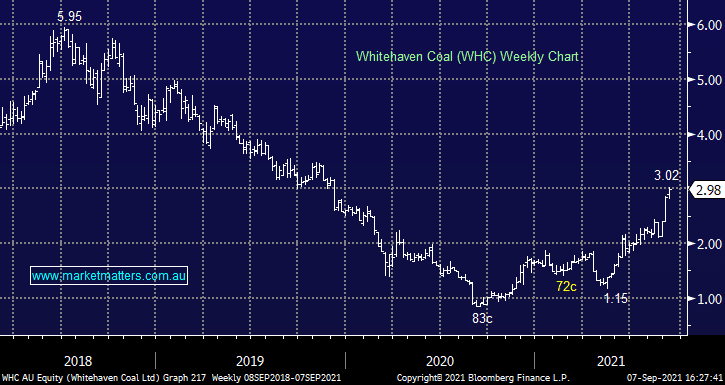

Peter O’Connor, our resource Analyst at Shaw sums up his current picks in the resource space this morning and I’ve included key highlights below. We own Whitehaven Coal (WHC) & Newcrest (NCM) in the Growth Portfolio + have had S32 on the radar for a while, although we now prefer to buy the consolidation of the ~$3 breakout. We also own Coronado Coal (CRN) in the Emerging Companies Portfolio which is aligned with these views. Click Here To View Portfolio’s

- Gold px poised to break higher – Price has been grinding higher post the June FOMC “taper tantrum” and the latest soft US payroll data likely to see gold push higher towards US$1,900/oz as the gap to US real rates closes. Buy gold.

- Met coal still a lot more catch up – The two best performing commodities YTD – met and energy coal. Yet the gap to China met prices is over US$100/t which combined with firm ex-China demand suggests further upside ~30%. Buy WHC, S32.

- Alumina cum 10% upside – Australian alumina price has been tracking China import parity price higher over the past 6 months. The gap has widened to ~$40/t (12%) prior to any Guinea cost input pressure. Buy AWC and S32.

- Bauxite at 18 month high – Supply concerns from major global exporter, Guinea, post Monday’s coup, will likely maintain price tension on bauxite in the near term. Buy Metro Mining, AWC, S32.

We remain bullish & overweight Commodities

Add To Hit List