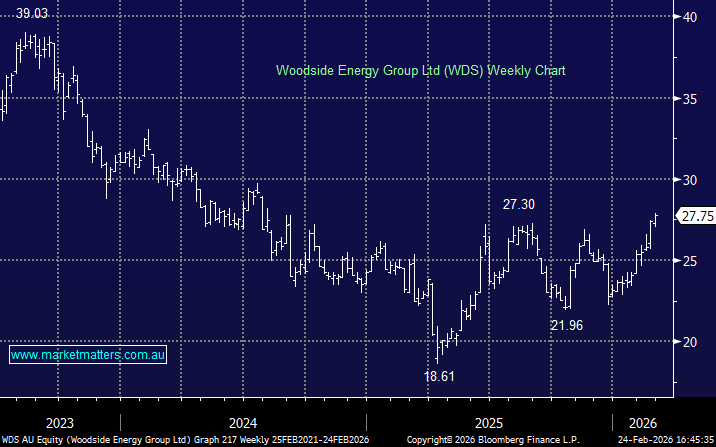

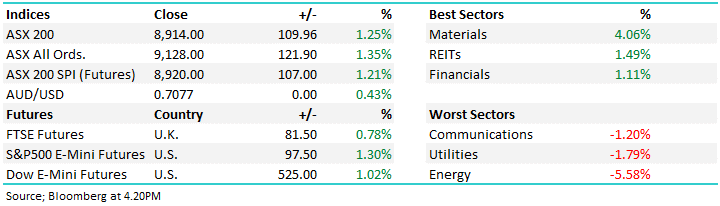

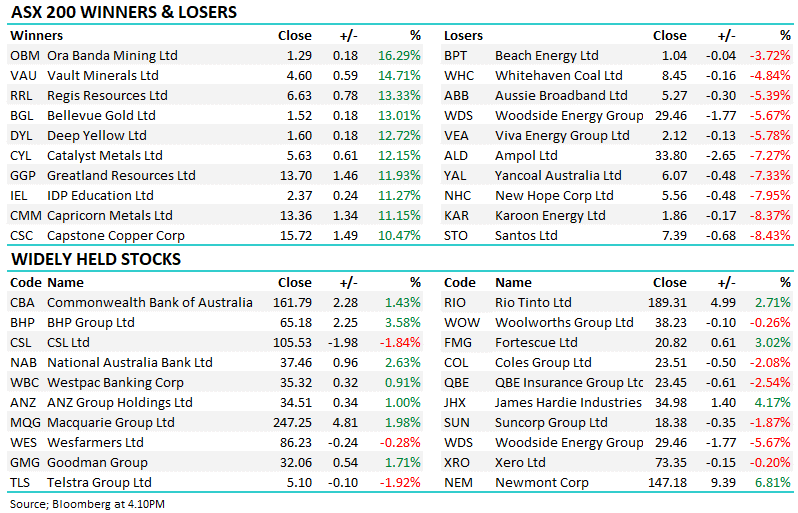

WDS +2.4%: A strong day on the back of rising oil prices, Woodside delivered a solid result with record oil production and a better-than-expected dividend catching a market that had been bracing for a more conservative stance given the heavy project spend underway.

1H26 Highlights

- Net income: US$2.7bn, -24% y/y

- Record total production 198.8mmboe, +6% y/y

- Average realised price US$60/boe, -5% y/y

- Final dividend US$0.59 (vs. US$0.53 y/y)

While profit declined on softer realised prices, higher production helped cushion the impact, with output reaching a record level. Project execution remains on track with Scarborough nearing completion (94% complete), Trion on track for 2028 and Louisiana LNG progressing toward first cargo in 2029.

The surprise uplift in the final dividend suggests balance sheet capacity remains comfortable even as capex peaks. If production can continue to trend higher from current record levels as Scarborough ramps and other projects come online, that should translate into stronger revenue and cash flow generation to allay the market’s main concern around sustainability of paying a reasonable dividend.

MM is bullish toward WDS

Add To Hit List