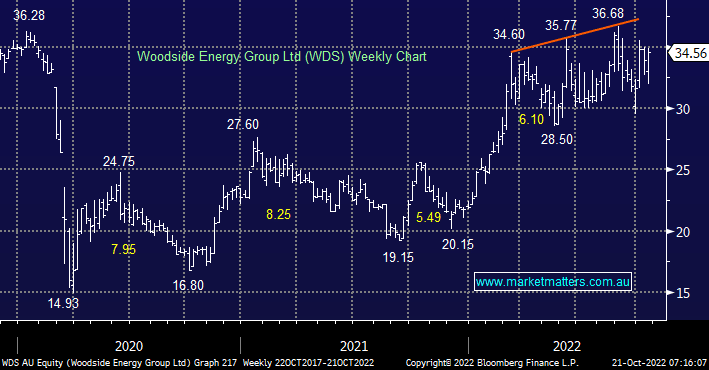

Yesterday saw WDS rally over +6% after it delivered record output for the September quarter with sales up 70% to $9.3bn thanks in part to the acquisition of BHP’s Petroleum division. Management also increased their full-year guidance in an excellent update which saw the market reward the strong performance. The company produced 51.2 million barrels of oil equivalent while guiding to an increase to 153-157 for its full-year definitely a case of so far so good after its major acquisition. The stock is currently trading on a 6.1x valuation for 2022 and a projected yield of 9.6% over the next 12 months with its next dividend due in February.

Revenue is forecast to rise from $16.1bn to $17.9bn in 2023 although its dividend is expected to slip from $2.48 to $2.21, even if it comes in 10% lower it puts the stock on a ~6% yield. Hence we see no reason to grab profits at current levels although the risk/reward does skew down closer to $38.

- We believe WDS can make fresh 2022 highs into Christmas.

MM remains bullish and long WDS

Add To Hit List