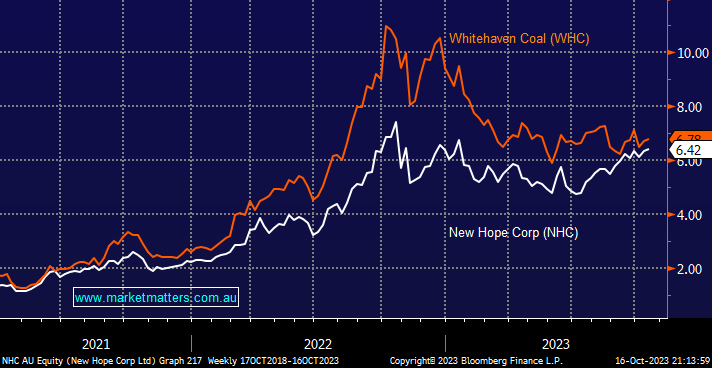

Two ASX coal companies with very different fortunes through 2023, WHC has fallen -28% while NHC has risen +2%, and that trend continued on Monday with NHC outperforming by +0.4% although both closed higher. The huge difference in relative performance has been driven by management-flagged direction over the coming years:

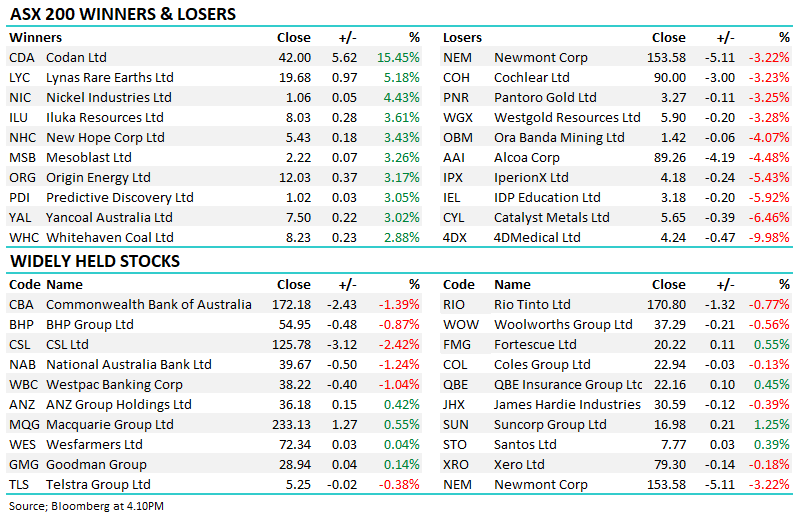

- Whitehaven Coal (WHC) $6.78 – is focusing on growth after suspending its buyback to bid for BHP’s QLD coal mines, with a price tag of ~$5bn the company looks set to disappoint investors in search of yield and capital management – we are long in our Active Growth Portfolio.

- New Hope Corp (NHC) $6.42 – have flagged future capital management will include fully franked dividends, on-market buybacks and other capital returns, i.e. almost the opposite to WHC – we are long NHC in our Active Income Portfolio.

We can see both stocks heading towards $7 into Christmas, but for WHC to start to outperform, we need to see the market adopt our more positive outlook toward fossil fuels over the coming years.

MM is long and bullish on both NHC and WHC

Add To Hit List