- Markets @ Midday: Listen here at lunchtime or find all Market Matters Podcasts on Spotify.

The ASX surrendered early gains and finished mildly lower after a hotter-than-expected December CPI reading firmed market expectations of a February rate hike from the RBA. The prospect of higher rates weighed most heavily on rate-sensitive growth stocks, while banks and energy provided partial offset as investors rotated toward beneficiaries of a higher-rate, higher-yield environment.

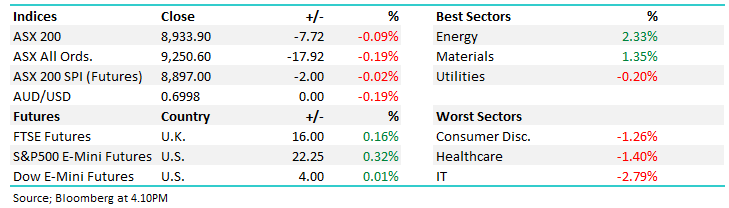

- The ASX200 fell -7pts/-0.09% to close at 8933.

- Energy (+2.33%) and Materials (+1.35%) the only two sectors higher.

- Technology (-2.79%), Healthcare (-1.4%) and Consumer Discretionary (-1.26%) weighed.

- 4Q Headline CPI was hotter than expected, but we still don’t think it’s hot enough to push the RBA to reverse course and raise rates next week.

- That goes against what markets are now pricing, with a 70% probability of a hike now factored in.

- Headline CPI was +1.0% MoM in December, pushing annual inflation up to 3.8% – well above the consensus estimate (3.6%).

- However, the seasonally adjusted CPI rose just 0.2% MoM (2.4% annualised). Excluding a transitory spike in July 2025, momentum continues to moderate toward the RBA’s inflation target.

- The RBA focuses on core inflation, which was in line with expectations, with the trimmed-mean CPI up 0.9% QoQ and 3.3% annual. That is higher than the RBA’s own forecast (3.2%) but not materially so.

- The AUD was above 70c on the print, and equities fell ~60pts from the high before both reversed some of the moves.

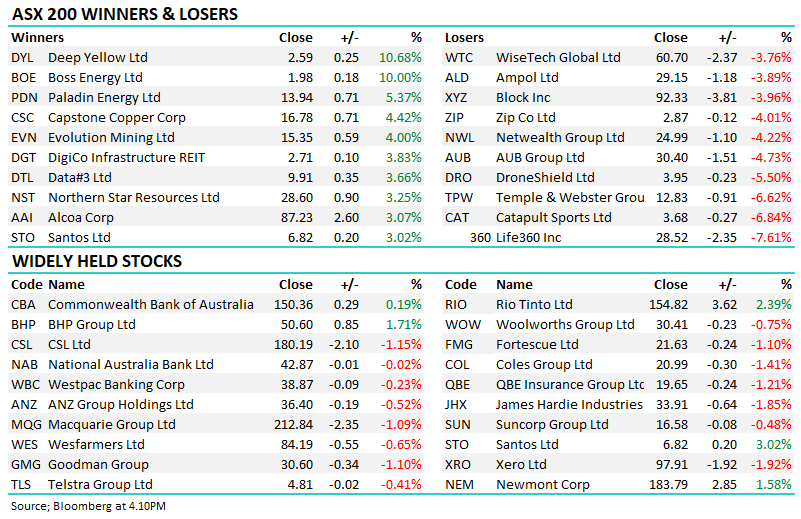

- NextDC (NXT) −2.7% and Life360 (360) −7.6% WiseTech Global (WTC) −3.7% weakened as the rate-sensitive growth cohort bore the brunt of the sell-off.

- Woodside Energy (WDS) +2.7% climbed after reporting record 2025 production and benefiting from firmer oil prices following US winter-storm disruptions. Santos (STO) +3% rose in line with its peer, and higher crude prices.

- Catapult Sports (CAT) -6.8% fell after it was revealed CEO Will Lopes sold 1.3 million shares on January 22 with proceeds used to fund the cost of exercising Catapult options – we’ve heard worse reasons for insider selling.

- Northern Star (NST) +3.2%, Evolution Mining (EVN) +4% and Regis Resources (RRL) +1.5% gained as gold extended its rally, offering a defensive offset in a rate-worried market.

- Deep Yellow (DYL) +10.7% jumped sharply as uranium stocks caught a bid overnight in the U.S, the nuclear energy story showing strong momentum.

- ASX Ltd (ASX) −0.3% slipped after lifting FY26 expense growth guidance to 13-15%, on higher spending for risk management and technology upgrades.

- Boss Energy (BOE) +10% surged after cutting cost guidance following a strong quarter at its Honeymoon uranium operation.

- Coronado Global Resources (CRN) −5.5% fell as investors took profits despite results coming in within guidance.

- AUB Group (AUB) −4.7% eased despite reaffirming guidance, completing a heavily discounted $400mn institutional placement.

- DroneShield (DRO) −5.5% drifted lower as CEO Oleg Vornik reiterated that part of his earlier share sale was to meet tax obligations – ~$60mn is a lot of tax!

- Gold was up ~$72/oz, trading at US$5250/oz around our close.

- Iron ore was lower, trading $US103.10/mt.

- Asian markets were higher, with China up +0.4%, Hong Kong +2.1% higher and Japan down -0.5%.

- US futures are trading up +0.3%.

- Big night tonight for reporting in the U.S with heavyweights Microsoft (MSFT US), META Platforms (META US) and Tesla (TSLA US).