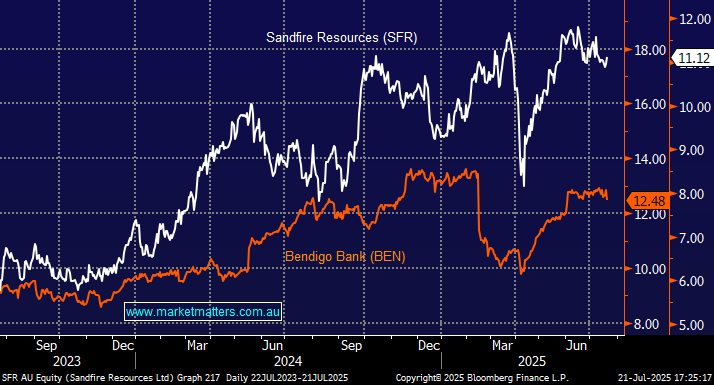

Unlike the other miners looked at today copper producer SFR has rallied over recent years and is now looking tired around its all-time high. Regional bank BEN has started to look interesting recently, ably supported by its 5% fully franked yield. Avoiding the regional banks has paid dividends across global markets through 2024/5 but BEN will pop onto our radar if we see weakness below $12, with the investment case helped by its relatively conservative valuation relative to an expensive banking sector.

- SFR – We are short-term neutral SFR between $11 and $11.50 but medium/long term bullish on copper stocks.

- BEN – We are initially targeting the $12 area, or another 4% lower.

No interesting performance rotation likely between these two.

- We can see SFR outperforming BEN over the coming weeks/months, primarily because the banks look vulnerable.

MM prefers SFR over BEN short term

Add To Hit List

chart

Sandfire Resources (SFR) v Bendigo Bank (BEN)

chart

Sandfire Resources (SFR) v Bendigo Bank (BEN)