In 2022, as is the case today, energy stocks led the market, with the US-Iran conflict helping the sector rally +27% so far this year. Energy remains the most direct inflation trade: company revenues rise with commodity prices, while much of the cost base is largely fixed, particularly where wells and mines are already developed, releasing a surge of free cash flow. However, there is another positive factor in play today: the enormous energy demand expected from AI.

While we know coal has a “half-life”, so to speak, as the world transitions toward cleaner energy, we believe a significant supply/demand gap is emerging over the next decade, driven in part by AI and the associated growth in electricity consumption. Coal is well positioned to help fill that void. Coal companies are currently generating strong earnings, trading on low multiples, and we think demand over at least the next decade will remain robust. India is a key part of this story, with the country expected to be the largest source of incremental coal demand growth through to 2030, driven by rising electricity consumption, steel production and industrialisation.

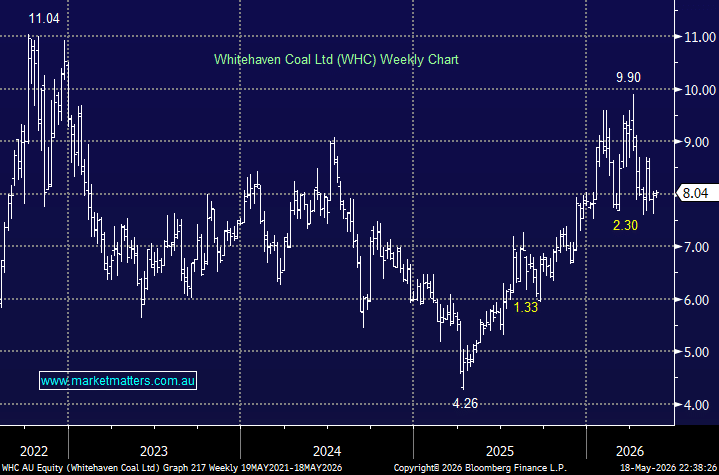

There are two main coal stocks on the ASX: Whitehaven Coal (ASX: WHC), which has skewed production more toward metallurgical coal used in steelmaking, and New Hope (ASX: NHC), which is more exposed to thermal coal used in power generation. Whitehaven is our growth pick, held in the Active Growth Portfolio, and New Hope is the choice for income, held in the Active Income Portfolio.

If we are entering a commodity Supercycle underpinned by significant investment in infrastructure — both physical and digital — a theme we have mentioned several times in recent reports and continue to believe is playing out, then commodities should be a cornerstone of portfolios, particularly in a higher-for-longer inflationary environment.

Obviously, there is a high degree of cyclicality in the commodity trade, and these stocks can often swing 20-25%. But, as they say, volatility is the price of admission!

In March, we trimmed our position in Whitehaven back to 4%, but we are still targeting the $11 area, making ~$8 an attractive risk/reward entry level in our opinion.

- We believe quality coal stocks, including Whitehaven, will outperform the ASX over the coming year.

MM is long and bullish on Whitehaven Coal around $8

Add To Hit List