MFG is preparing to consign one of Australia’s best-known investment brands to history, with the combined business set to become Barrenjoey Group following completion of its $1.62 billion merger with Barrenjoey Capital. Subject to shareholder approval in October, it will trade under the new ASX ticker BJY, while Magellan Investment Partners will become Barrenjoey Investment Partners. Completion is expected in early July following ACCC clearance.

The change goes well beyond a new name. Magellan is also reducing its reliance on traditional fundamental funds management, appointing quantitative manager Vinva to run approximately $5.3 billion across its flagship global strategies. Management fees will fall from 1.35% to 0.89%, or around 0.80% after Vinva’s sub-advisory fee, while performance fees will be removed and the internal global-equities team substantially reduced. The changes are expected to lower annual revenue by around $30 million and reduce pro-forma group earnings by approximately 8%.

While painful in the near term, the reset is designed to address the underperformance and persistent outflows that have plagued the legacy Magellan business. Vinva has delivered a stronger recent investment track record, while the lower fee structure is more competitive and may help stem retail redemptions over time.

The transition also highlights how dramatically the earnings mix is changing. By FY27, traditional investment management is expected to account for only around 15–20% of pro-forma earnings, leaving Barrenjoey and the group’s other investments as the primary drivers of value.

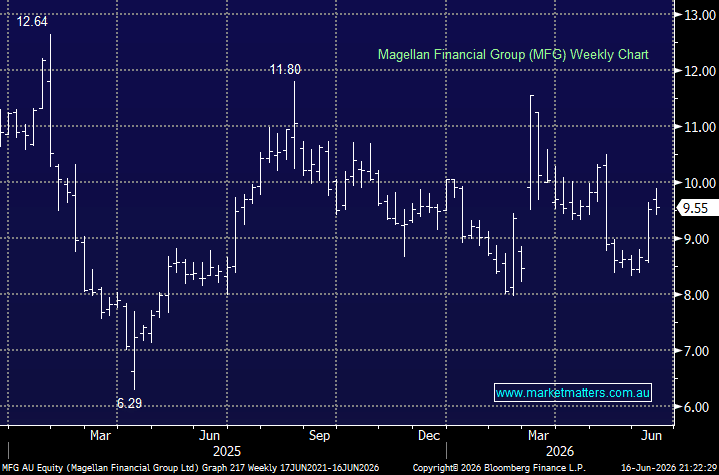

Longer-term subscribers will understand our history with Magellan across both the Income and Growth portfolios. While we have experienced some pain investing in MFG, it has actually been a reasonable performer overall. We have made money from the stock at various times since 2020—approximately 9% in the Income Portfolio and 28% in the Growth Portfolio.

That said, the shares have generally trended lower since peaking near $75 in 2020, eventually reaching $6.29 in November 2025. With the stock now trading in the mid-$9s and a genuine fresh start in the offing, the question is whether we should become interested again.

MFG looks relatively cheap compared with the broader market, although most listed fund managers do. At around 13.7x forward earnings, it actually screens in the upper quartile of the approximately 20 listed managers we cover. However, that comparison is becoming less relevant given the group’s substantial cash balance and the very different structure emerging from the merger.

Many investors are describing the combined business as a “mini-Macquarie”—a diversified financial-services platform spanning investment banking, markets, funds management and strategic investments. Macquarie trades on around 19x earnings, suggesting Barrenjoey has scope to deliver both earnings growth and a higher valuation multiple if management executes successfully. That combination could meaningfully amplify shareholder returns.

The transaction draws a line under the old Magellan and shifts the investment case away from repairing a damaged funds-management franchise toward building a broader financial-services platform. Barrenjoey brings a strong position across mergers and acquisitions, equity capital markets, institutional equities and research. Its dealmakers have started 2026 strongly, ranking third in Australian-related M&A after advising on transactions worth approximately US$12.9 billion.

The opportunity is credible, but risks remain. Around $3.7 billion of institutional global-equities mandates could be reviewed following the changes to investment strategy and personnel, creating further redemption risk. Investment-banking earnings are also cyclical and can be volatile. The next phase is therefore likely to focus on adding more stable, recurring revenue streams through acquisitions and expansion into adjacent markets, potentially including New Zealand and Asia.

There is also substantial integration work ahead. The combined group is expected to remove overlapping roles across technology, marketing and finance, with job losses likely to fall disproportionately on the Magellan side. Management must also navigate potential conflicts between its investment-banking and asset-management operations, while determining whether non-core investments such as FinClear still fit the strategy.

Retention is another key risk in a people-driven business. However, the merger includes lengthy restrictions on senior Barrenjoey shareholders. Matthew Grounds and Guy Fowler are locked in for nine years, while other key staff generally face restrictions of between three-and-a-half and five years, helping protect the franchise through the integration period.

There has been no firm dividend guidance or formal payout policy announced for the combined group. That is probably deliberate: Barrenjoey is more capital-intensive and cyclical than the legacy Magellan business, while management appears keen to retain flexibility for acquisitions and expansion.

Magellan’s existing policy is to distribute at least 80% of investment-management operating profit after tax, subject to capital requirements and strategic priorities. Current forecasts imply a dividend of around 64–65 cents for FY26, although we suspect the combined group’s FY27 distribution could be closer to 50 cents, implying a yield of approximately 5% at current prices.

- Overall, we believe MFG has a stronger future under Barrenjoey, although the near-term integration challenges will take time to play out. We are adding MFG to the Income Portfolio Hitlist as a potential replacement for the underperforming GQG Partners (GQG).

MM is cautiously bullish MFG ~$9.50

Add To Hit List