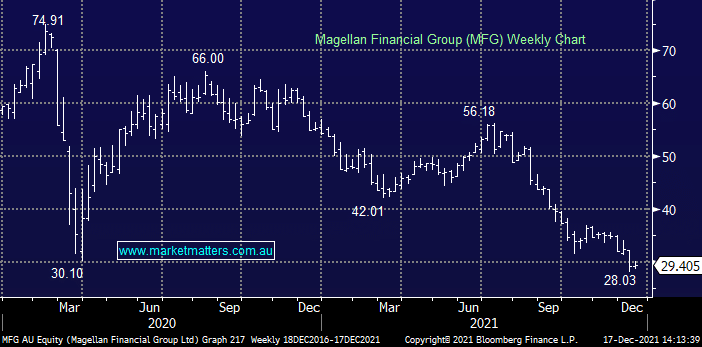

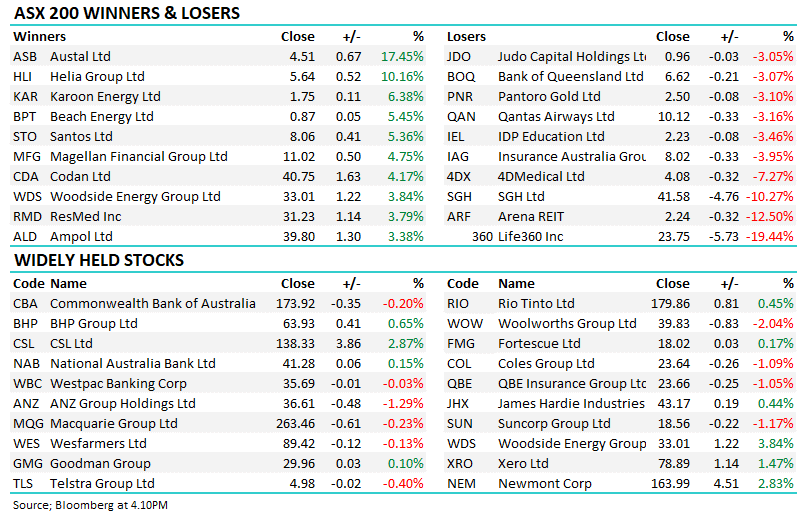

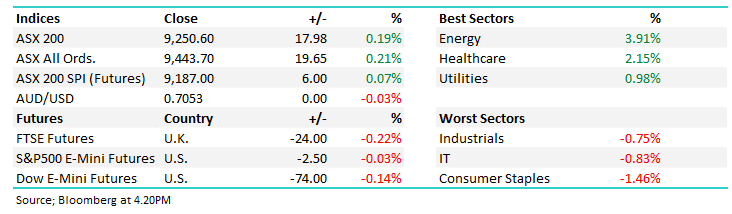

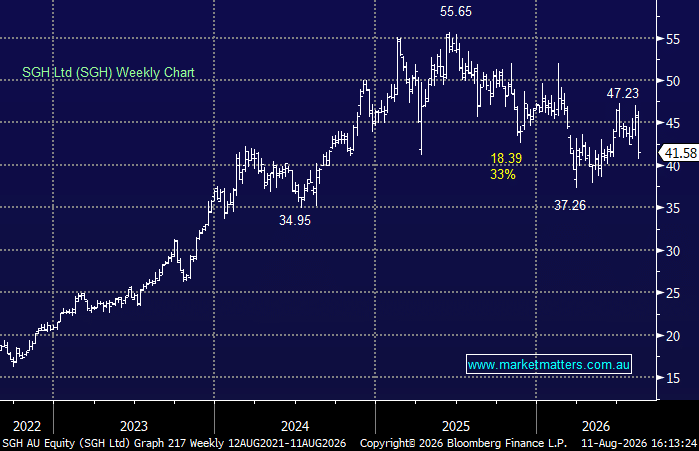

Boral & Magellan under the microscope

Hi James and team, Thank you for your services--its been a fairly good year due to your astute observations and comments. Thanks again. A couple of questions please when you are able: MFG-I have been a happy holder of MFG for some 7 plus years, but my loyalty (especially) to the “Hamish factor” is looking a bit misplaced by now, and I read from company docs that there are structural changes ahead which may make it Impossible for MFG to repeat its performances of the past good years--specifically tax changes --" , investors should also be mindful that MFG is subject to higher taxes in three years' time (from the concessional 10% towards a 30% tax rate), following an end to special tax breaks on offshore banks and fund managers. Although this may mean more franking credits, it also reduces the potential for MFG to sustain its dividend yield” . and also some inferences that there may be some disagreements at top management level, and worries about structural/negative changes to be caused by recent Chinese government policy changes. BLD--Has been divesting itself of US assets steadily--but still has about 3 bill AUD to come in if I read the reports correctly. From what I read in Chairman’s report, this is to “distributed to shareholders” --when they figure out the best way to do it (my understanding) ---However the continual “South East” trajectory of the share price is not what I would expect at all--I would have though at least some “North East” travel-- lol…What (probably obvious) thing am I missing here??--Is all the news already in the price?? Merry Xmas and a Happy New Year, Kind Regards Paul A.