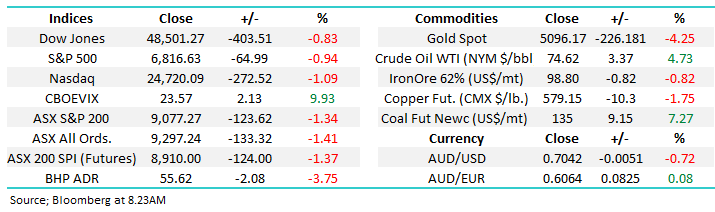

The ASX was hit today, unwinding yesterday’s strong recovery from the lows, with commentary from RBA Chair Michelle Bullock at an AFR event dovetailing into higher oil prices driving a sharp increase in local bond yields on firming rate hike expectations at the next meeting.

Higher oil prices are inflationary, and the market was previously positioned for a pause at the next meeting on the 16-17th March, however after today’s comments + the flare up in Iran driving higher oil prices, the market moved to pricing a ~30% probability of a hike in March, and fully pricing a hike in May (for the first time).

That saw equities sold down aggressively from around midday onwards, finishing near their lows.

- The ASX200 fell -123pts/-1.34% to close at 9077

- Energy (+1.41%) & Consumer Staples (+0.02%) the only sectors to make gains.

- Materials (-3.09%), Consumer Discretionary (-2.8%) and IT (-2.17%) weighed.

- New Hope (NHC) +7.4% rallied as Newcastle coal futures jumped 8.6%, with investors positioning for stronger near-term earnings leverage if LNG outages force utilities back toward thermal coal. They also extended their on-market buy back.

- Yancoal (YAL) +4.9% & Whitehaven Coal (WHC) +3.2% – rallied for the same reason, though NHC has most relative exposure to Thermal Coal.

- Woodside Energy (WDS) +0.8% and Santos (STO) +1.0% rose modestly after strong gains Monday, supported by firmer oil but capped by broader equity weakness.

- Ampol (ALD) +3.2% outperformed as refining margins and retail fuel spreads will benefit from volatility in crude markets

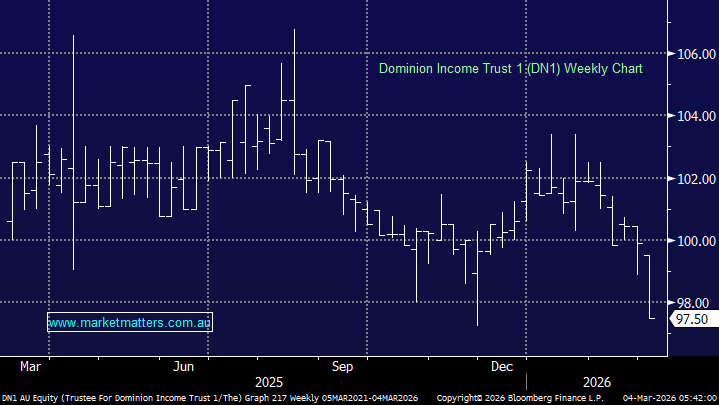

- Fixed income manager Realm has confirmed they have $80m exposure to collapsed lender MFS in their Strategic Income Fund. The Dominion Notes (DN1) have 0.5% of their portfolio exposed to MFS on a look through basis, however they have an equity buffer that will handle the impact. The worst-case scenario for the Strategic Income Fund is a loss of ~2.2%. DMNHA has no exposure (but was sold off anyway). We will cover this in more detail in tomorrow mornings note, given the Income Portfolio owns DN1.

- DMNHA fell -2% today, while DN1 was off 1.3%. Other private credit managers were unaffected for now.

- Newmont (NEM) -2.0%, Northern Star (NST) -3.2% and Evolution Mining (EVN) -4.5% all fell, implying the stocks are crowded into new highs – we sold Newmont.

- Qantas (QAN) -1.8% fell to its lowest close since May amid ongoing Middle East flight disruptions and concerns over higher jet fuel costs.

- DroneShield (DRO) -6.2% retraced Monday’s strong gains as punters locked in profits.

- Magellan Financial (MFG) +21.9% surged after completing a $130m placement at $8.45 to fund its merger with Barrenjoey, with investors betting the deal accelerates earnings diversification and growth.

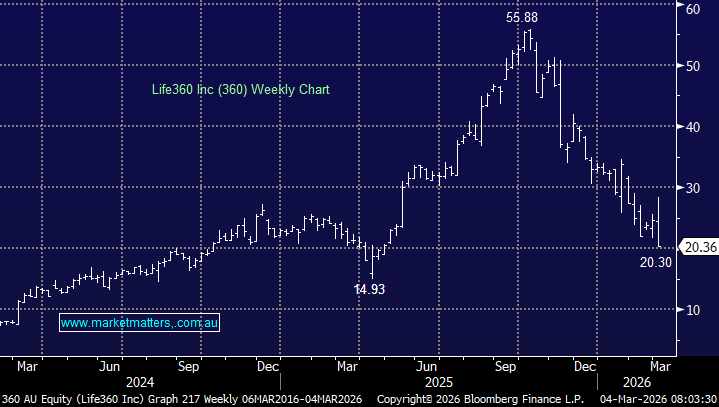

- Life360 (360) –17.6% was hit hard despite headline results coming inline with expectations – 1Q EBITDA margins lower on front-loaded marketing spend, overshadowing its maiden annual profit. The stock was higher on open – big reversal lower as the day progressed.

- Stockland (SGP) –2.2% dipped after finalising its 50/50 data centre JV with EdgeConneX, though we suspect this is more macro (interest rate) related.

- Capstone Copper (CSC) -8.1% declined despite record revenue as adjusted EBITDA missed expectations, prompting concerns over cost pressures.

- Looking at the MM Portfolios today, Growth dipped ~0.8%, Income down ~0.7%, Emerging Companies fell ~1.2% and Core ETF was off ~0.7%.

- Iron ore was down ~0.9% at $US98.35/mt

- Gold has just fallen ~$75 in a matter of minutes, now trading at US$5300/oz

- Asian markets were down; China -1%, Hong Kong -0.9% and Japan fell -3%.

- US futures are trading down ~0.8%