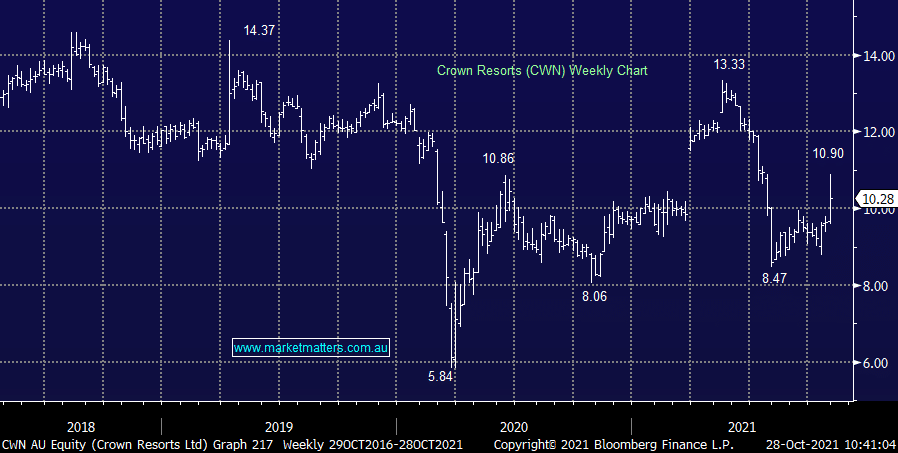

We are selling our 4% holding in Crown Resorts (CWN) today, taking a small profit. While we could look ‘stupid’ pretty quickly if CWN is taken over, we simply believe the conditions to retain the license are onerous enough to imply a very slow and protracted recovery. We can scratch the position for a small profit now & re-asses later on.

MM are selling CWN in the Flagship Growth Portfolio, taking a small profit around $10.25

Add To Hit List

We are buying Resmed (RMD) into recent weakness. This is a high quality, somewhat expensive healthcare company that has defensive earnings – adding quality into weakness generally pays off.

MM are buying RMD in the Flagship Growth Portfolio, allocating 4% around $35.64

Add To Hit List

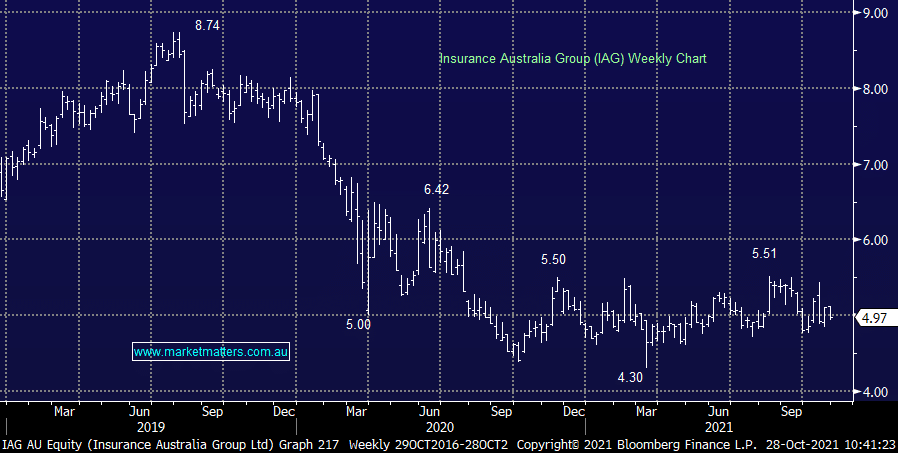

We are selling our 4% holding in IAG Insurance (IAG) in the Flagship Growth Portfolio only. We believe QBE has better growth potential which aligns more accurately with this portfolios objective.

MM are selling IAG in the Flagship Growth Portfolio only, taking a small loss around $4.97

Add To Hit List

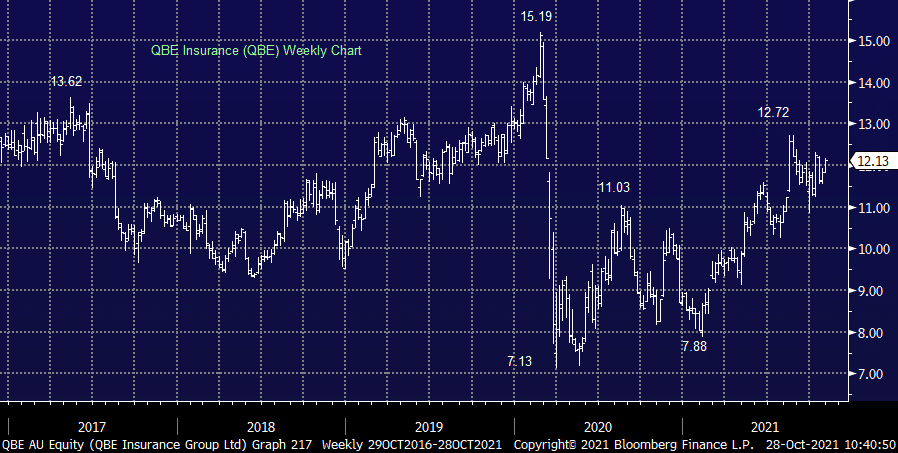

We are buying QBE Insurance (QBE) to take advantage of rising US bond yields and an improving operational outlook from the global business. We view QBE as a better growth orientated option in the Insurance space than IAG, although we remain comfortable IAG for yield.

MM are buying QBE in the Flagship Growth Portfolio, allocating 4% around $12.15

Add To Hit List