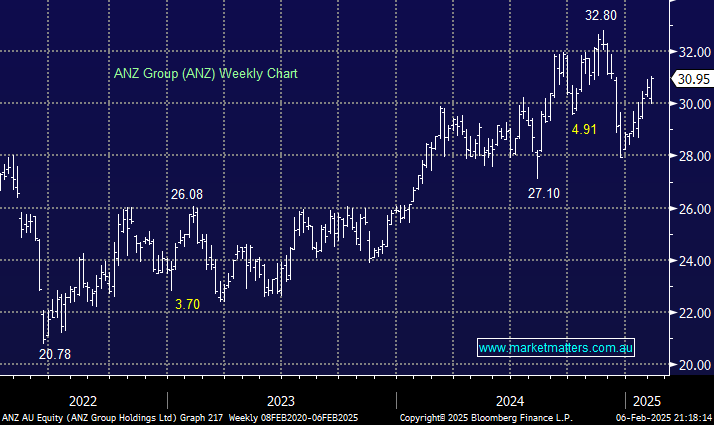

ANZ was the best of the banks on Thursday rallying +2.6% but it was the only one of the “Big Four” not to post all-time highs – a sector laggard outperforming. From a valuation perspective, ANZ remains our preferred option, coming off a lower base and with more room to improve earnings post Suncorp acquisition. Dividends are often sighted as the reason to buy/own the banks, and ANZ is attractive at 5.7%, however, as we’ve seen this year, capital gains can also be meaningful when the market gets wrong footed by stronger than expected bank earnings.

We continue to believe beneficiaries of lower rates, such as ANZ should trade well through 2025 unless Michele Bullock plays the Grinch.

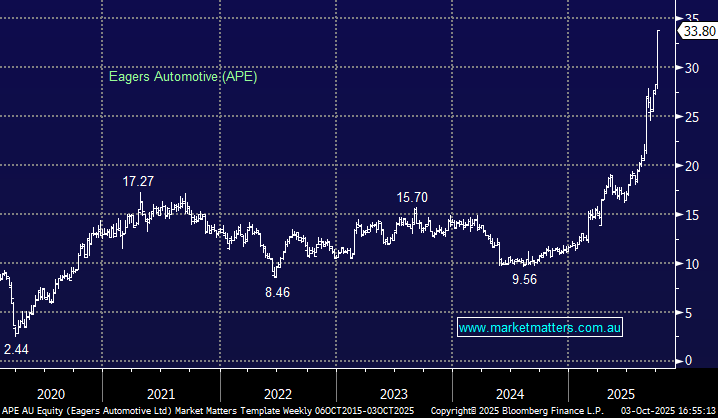

- We remain bullish ANZ initially targeting the $33-35 area; we don’t expect the banks to lead the market in 2025, although they did yesterday, its just hard to justify selling them given earnings momentum and yield; MM holds ANZ in its Active Growth and Income Portfolios.

MM is long and bullish ANZ

Add To Hit List