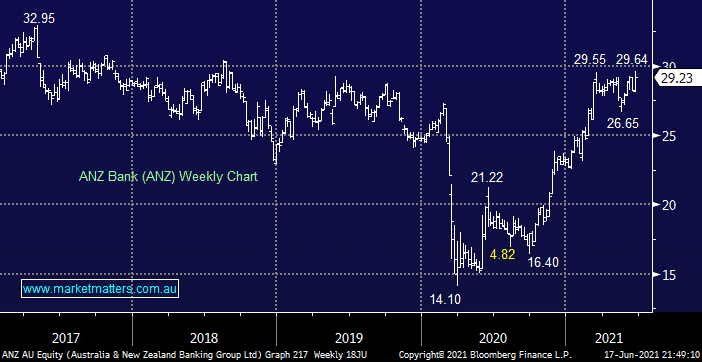

Commonwealth Bank (CBA) is garnering most of the headlines for the Australian banks as it soars above $100 to fresh all-time highs. However the whole sector is coming along for the ride as higher bond yields should produce improved margins for the sector, plus of course they are now incredibly well capitalised and primed for capital management as COVID provisioning unwinds. ANZ Bank (ANZ) for example has more than doubled from its COVID panic sell off but from a risk / reward perspective we wouldn’t now be keen buyers until we witness a ~8% pullback.

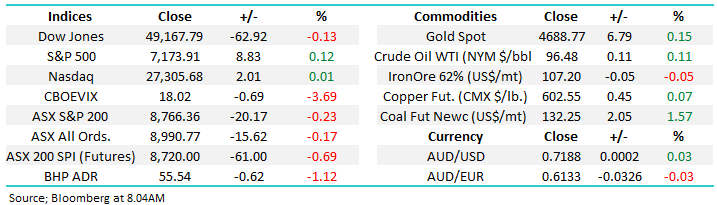

Yesterday’s unemployment data showed the Australian jobless rate has fallen back to its pre-pandemic level of 5.1% with the current momentum implying it has further to go. The RBA is going to find it hard to ignore the improving domestic economic data plus a Fed which intends to hike rates twice by the end of 2023, local futures traders are currenting positioned for a local increase by late 2022, currently a more aggressive stance than Philip Lowe. The RBA’s rhetoric remains focused on inflation and wages growth, the latter would need very low unemployment to be achieved and importantly, once the inflation genie is out of the bag history has shown us It can be tough putting it back in.

MM is bullish ANZ liking the risk / reward back under $27

Add To Hit List