Toll roads, pipelines, electricity networks and airports often have revenues contractually linked to CPI. They are textbook inflation hedges: cash flows rise with inflation, asset values increase in replacement-cost terms, and the essential nature of the assets helps protect volumes. The caveat is that they are also rate-sensitive and can behave like long-duration bonds from a valuation perspective. If rates rise sharply, multiples can compress in the short term, even if underlying cash flows remain resilient. That said, we believe portfolios should have an allocation to this space as we head into EOFY.

Private equity again showed its appetite for the sector in April, with IFM bidding for global toll road owner and operator Atlas Arteria (ASX: ALX).This follows Spark Infrastructure being acquired in 2021 by KKR, Ontario Teachers’ Pension Plan and PSP Investments, while Sydney Airport was privatised by IFM in 2022 in one of Australia’s largest-ever infrastructure deals.

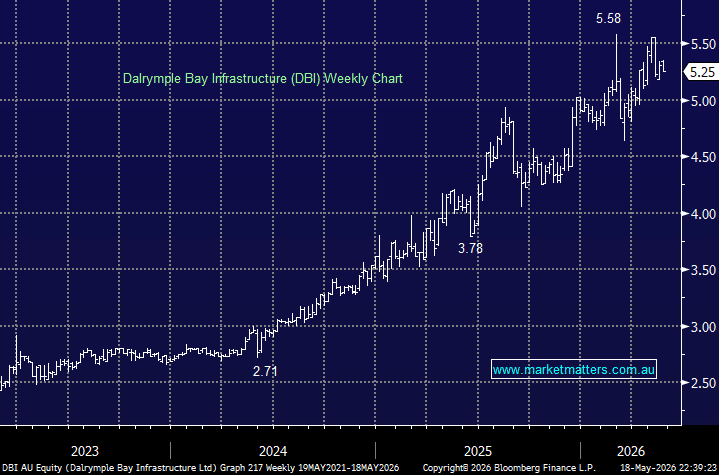

- Unfortunately, there is no longer a smorgasbord of high-quality infrastructure assets left on the ASX, and we already own two of the best ones: Dalrymple Bay Infrastructure (ASX: DBI) and APA Group (ASX: APA).

Dalrymple Bay Infrastructure owns and operates the Dalrymple Bay Coal Terminal in Queensland. Importantly, DBI is not a coal miner; it is better thought of as an infrastructure-style toll-road business. While DBI is not immune to a long-term decline in coal, its cash flows are considerably more stable than those of a typical miner and are more closely tied to export infrastructure utilisation than short-term coal prices.

- We believe Dalrymple will continue to outperform the ASX in the coming year, supported by CPI-linked price escalation in its core contracts, supporting ongoing growth in yield – which currently sits ~5% (and growing). MM owns Dalrymple in the Active Income Portfolio.

MM is long and bullish Dalrymple around $5.25

Add To Hit List