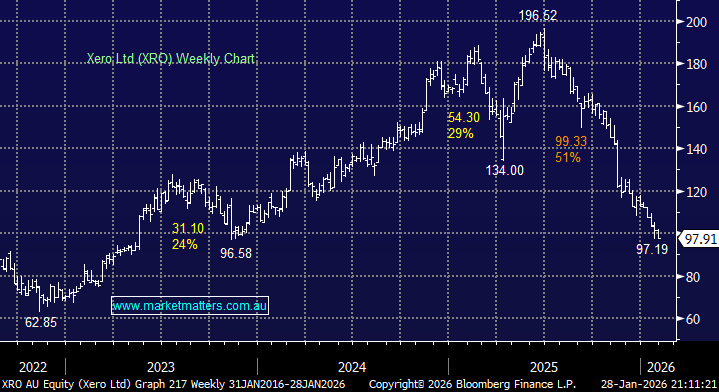

The $16.6bn NZ-based accounting software business has gone from hero to zero in just eight painful months. There have been a few issues here compounding the general AI-driven sell-off across the software space:

- The stock was, and still is, trading on a very high valuation; currently it’s on an 82x basis March’26 FY, which is actually 60% below its 5-year average and falling.

- In late 2025, XRO bought Melio for US$2.5bn, a US B2B payments platform, a strategic move to scale its presence in the North American market and broaden its software and payments offering, a deal which looks very expensive in the current environment.

In many ways, Xero (XRO) still looks expensive, reflecting a combination of valuation, execution risk and elevated investor expectations. Top-line growth has naturally slowed as the business scales, and software incumbents typically de-rate once organic growth moderates — particularly in mature markets like ANZ, which helps explain Xero’s push into the US. The issue is that Xero continues to trade on premium multiples built on strong growth assumptions, yet growth has cooled, profitability is still emerging, and the market is demanding proof that major strategic bets — particularly Melio — will deliver. In the current environment that punishes long-duration growth stocks, and with AI adding fresh uncertainty around software moats, there’s simply less margin for error and investors have acted accordingly.

Compared to the $US150bn US giant Intuit, its direct competitor, XRO, also looks expensive, but it is still growing faster. With revenue forecast to hit $3.2bn in FY27, its healthy operating margins can easily remove these valuation concerns if Melio proves a prudent acquisition, albeit apparently poorly timed. At MM, we believe Xero’s moat remains real, driven by a sticky small-business customer base, ecosystem and recurring revenue, but the rise of AI compresses the edge. If Xero successfully embeds AI into its core workflows and adviser tools, it can reinforce and even extend its moat. If it lags, the moat becomes shallow, as competitors replicate core features quickly. From an AI risks perspective, this isn’t too bad, and we feel the current sector rerating is delivering an opportunity in XRO.

XRO can use AI to automate bookkeeping, invoicing, cash-flow forecasting and compliance, making its product even stickier. It can also power better adviser tools and services for accountants — a key retention anchor, and supercharged integrations and plugins may make the platform harder to leave. In FY25, XRO enjoyed over 40% of its revenue internationally, primarily in the UK, with the US as its focus of growth. If it can successfully integrate Melio in the business and grow US earnings, the stock is even looking cheap!

- We believe XRO can successfully grow earnings in the US via Melio, which focuses on small business payment solutions, and strategically complements Xero’s SMB-centric accounting platform.

MM is long and bullish XRO around $98

Add To Hit List