We heard yesterday that online accounting platform Xero (XRO) has made a significant $4bn move on American accounting and payments platform Melio Payments to help the ASX software giant gain scale in the lucrative North American market, something they have struggled with over the past decade. Melio makes accounting software for small and medium-sized businesses (SMB’s), importantly, with integrated payment options that help to simplify B2B payments i.e. improving efficiencies around accounts payable and receivables, which is the element Xero will integrate into their own platform.

The deal, which is XRO’s largest to date, will almost triple its North American revenue. Well respected XRO CEO Sukhinder Singh Cassidy summed up Xero and many other companies’ attitude, whether in payments or mining around acquisitions:

- “Payments is a very specialised space. We don’t believe we could have built it fast enough, and it would take years to acquire the kind of scale, expertise and customer traction that Melio has,” and “The US is far too competitive a market for us to wait that long to build it ourselves.”

We like the acquisition, believing it makes strategic sense to avoid missing the proverbial boat into the US market. Melio can provide XRO instant scale, important payments technology, and a better overall platform to compete with the US giant Intuit (INTU US). They paid a high price for a quality business, 13x revenue (Melio does not make a profit), but as we’ve witnessed all year, quality comes at a cost. Sukhinder knows this market very well, and since taking over in February 2023, the market has embraced her leadership.

The acquisition will give XRO full money movement workflow, allowing it to compete with INTU, which is very important. The other important aspect here is Melio’s syndication network, which embeds its B2B payment infrastructure into third-party platforms—such as banks, financial institutions, and vertical SaaS providers—allowing them to offer Melio’s payment services under their own branding. This means other brands are growing Melio’s under base, which currently drives 35% of its revenue, is the differentiator versus other payment solutions, in XRO’s view.

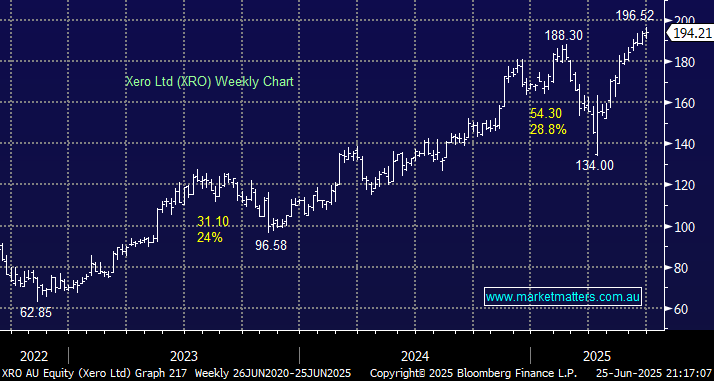

- XRO has completed the A$1.85bn institutional placement at $176/sh, and trading will resume this morning. There will be a $200m share purchase plan available for existing holders, while the balance of the funds were raised through debt and issuance of equity in XRO.

The stocks is likely to retreat when it resumes trading this morning, which may put it back on MM’s radar after we took profit this month at $193.50.

The acquisition price seems a bit high for the standalone business, but it works if the company can achieve strategic synergies through the greater distribution of both products and leveraging Melio’s payment technology through the XRO platform. While there’s much to like in the deal, we must also be conscious that it will take time to process the intricacies of the agreement and the pathway forward.

- We like XRO’s move to bulk up its US exposure with a leading, fast-growing payments player, illustrating the value of quality payment solutions.

MM would get interested in buying XRO again below $180

Add To Hit List