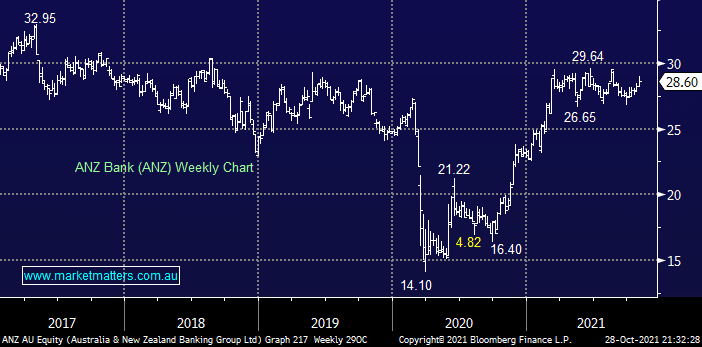

Yesterday saw ANZ deliver a solid result with cash profit up to $6.5bn aided by previous over provisioning for bad debts i.e. things haven’t been too bad through COVID. They’ve struggled to grow home loans over the last 12-months but that might not be a disaster if rates surge next year. Costs were a tad higher but nothing too disturbing and overall it was a good result, a beat in broking terms with importantly improved net interest income – the stock encouragingly rallied 0.74% on a down day for the ASX200.

Also, the bank will pay a 75c fully franked dividend on the 8th of November, the estimated yield for ANZ over the next 12-months is now 5.24% when grossed up for franking. MM is still anticipating a trading range between $27 and $31 into Christmas and we may consider tweaking our sector exposure accordingly.

MM is net bullish ANZ

Add To Hit List