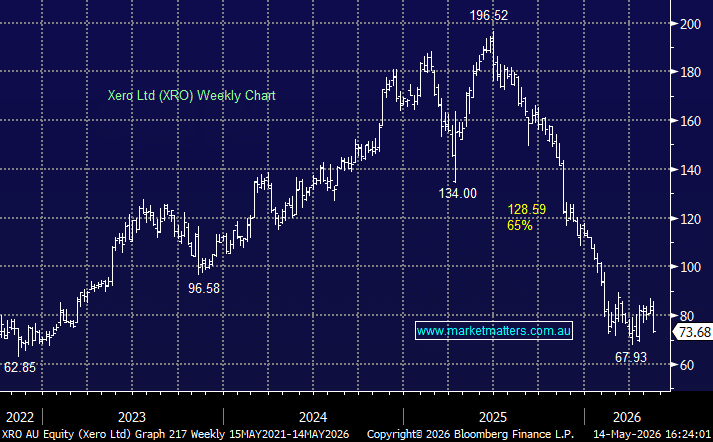

XRO -9.04%: reported FY26 results this morning that on the face of it, were solid, and a shade above consensus, but as the day wore on, the sellers got stuck in, looking beyond the headline earnings beat, focussing on profit quality, FY27 reinvestment, Melio-related noise and rising AI-related competitive risk.

FY26 Highlights

- Operating revenue: NZ$2.75bn, up 31% YoY, broadly in line with consensus at NZ$2.73bn.

- Annualised monthly recurring revenue: NZ$3.27bn, up 37% YoY.

- Subscribers: 4.92m, up 11% YoY, ahead of expectations of 4.88m.

- Net subscriber additions: +506k versus +254k last year.

- ARPU: NZ$55.44, up 23% YoY, ahead of expectations of NZ$48.77.

- Adjusted EBITDA: NZ$757.4m, up 18% YoY, ahead of expectations.

- Free cash flow: NZ$554m, up 9.3% YoY, well ahead of expectations of NZ$440.8m.

- Net income: NZ$167.4m, down 27% YoY, below expectations of NZ$232.1m – higher interest costs and tax rate to blame here.

- Operating expense ratio: 72.4% of revenue, versus 71.8% last year.

- Excluding acquisition-related costs, the operating expense ratio was 70.5%, in line with guidance.

For the year ahead, they guided to adjusted EBITDA between NZ$860m and NZ$920m (consensus was $860m), but they also said earnings would be more second-half weighted than usual.

The result itself was not bad. Revenue growth was strong, subscriber additions were better than expected, ARPU was robust, and free cash flow was materially ahead of consensus. That underpinned strength early – the headline numbers were a beat, but as always, the devil is in the detail. Net profit missed and was lower year on year, largely due to Melio-related acquisition costs, higher interest and higher tax.

Melio remains central. Strategically, the acquisition gives Xero a much larger opportunity in the US bill-pay and payments market, and the early growth is encouraging. However, the acquisition is also adding complexity, cost and integration risk. In the near term, it makes the reported numbers messier, even if the longer-term strategic logic is sound.

The other issue is AI. Accounting software companies are increasingly being questioned on whether AI tools will enhance their platforms or disrupt them. Xero is clearly leaning into the opportunity through partnerships with major AI providers and its own XeroForce product, but the market is not yet convinced. The concern is that AI-native tools could reduce the value of traditional accounting software over time, particularly for small businesses.

Overall, this was a good operating result, confirming that Xero continues to grow strongly and generate cash. That said, it did nothing to eliminate concerns around AI, and that’s the market key concern right now. This will take time to play out.

MM remains patiently long XRO in the Growth Portfolio

Add To Hit List