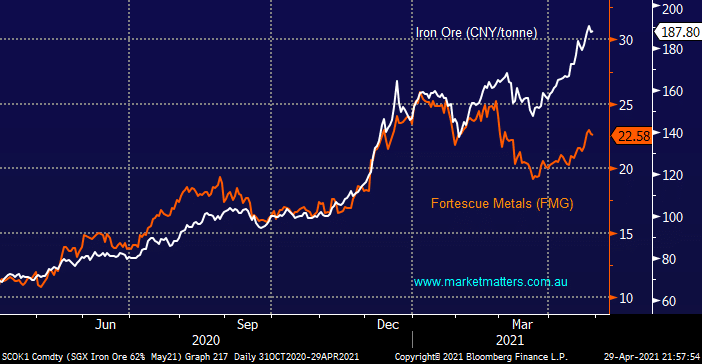

The iron Ore price continues to post fresh multi-year highs belying the many doubters who have been calling a top for the bulk commodity basically since I can remember. It’s a simple scenario to comprehend, post COVID the world is aggressively stimulating their economies led by China from an iron ore consumption perspective and until the spending pump is turned off iron prices should enjoy this significant tailwind.

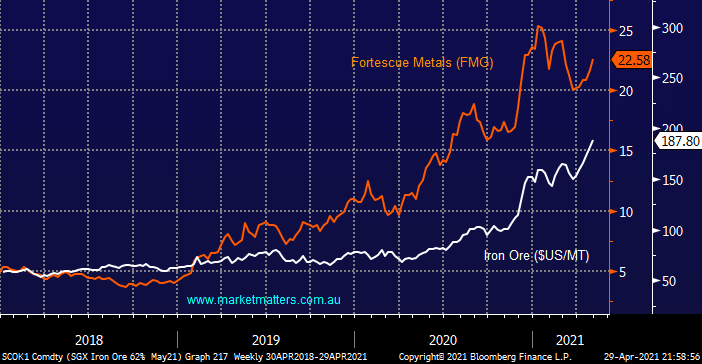

Interestingly Australia’s primary pure iron ore producer FMG has corrected over 20% even as the underlying commodity pushed ever higher, although it did pay a whopping $1.47 fully franked dividend in mid-February. Usually we would back the stock to be leading the commodity but in this case MM feels that investors keep underestimating how much money the likes of FMG will make with iron ore at current prices. The correlation between FMG and iron ore over recent years illustrates that stock has outstripped gains by the bulk metal but until China can satisfy its needs elsewhere (which they are working hard to do) FMG still looks fundamentally good value into any pullbacks.

MM is bullish FMG medium-term

Add To Hit List

However when we look at the correlation between FMG and iron ore over the last few months the picture is very different with the stock failing to embrace recent gains in the commodity, our current preferred scenario is some catch up by FMG probably back above $25.