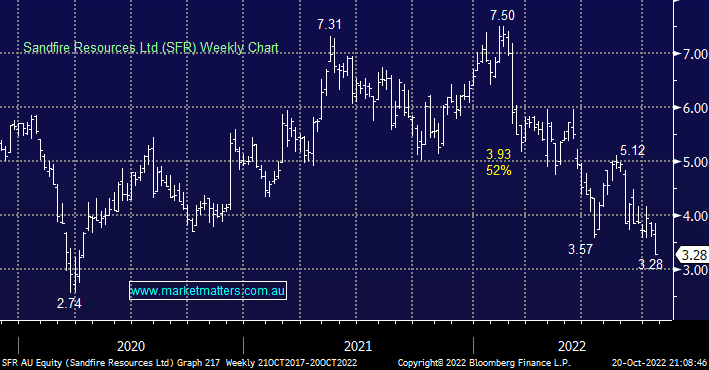

Yesterday saw copper miner SFR plunge over -13% after they delivered a weaker-than-expected Q1 result – lower production pushed up costs, an issue which has been witnessed across a few miners this year. Unfortunately, now this leaves SFR heavily reliant on a strong 2H to achieve full-year guidance, not ideal when we own it in our Flagship Growth and Emerging Companies Portfolios. We had previously considered adding to our holding sub $3.50 but for now, we aren’t prepared to fight this trend, but we will give this position more room given our medium term bullish stance towards copper.

- We no longer have any intention of increasing our exposure to SFR.

MM is now cautiously bullish and long SFR

Add To Hit List