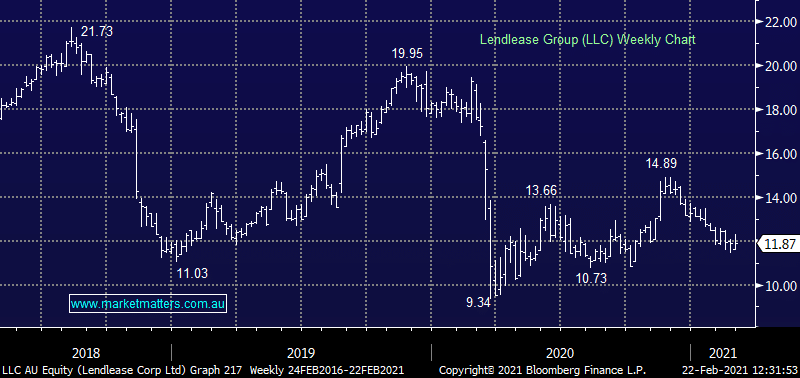

Underwhelming update today even against low expectations. Core NPAT at $205m was 7.6% below the $222m expected while the dividend of 15cps was pretty much in line. The building / construction segment was strong, the development and investment management area was not and provided the biggest drag on the result today. They did talk up their pipeline, although that’s pretty common, and as usual they provided no guidance. We like the the underlying dynamics that should be supportive of LLC, i.e. infrastructure spend, however as was the case with Cimic and a few other companies in this sector, time frames are blowing out.

For FY21, the market is forecasting NPAT of $471m.

MM remains bullish LLC

Add To Hit List