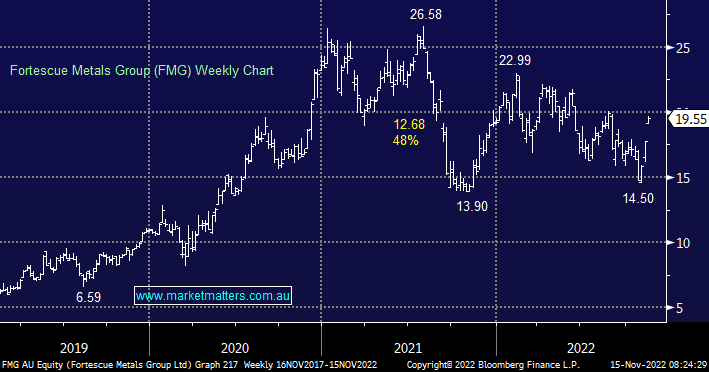

Fortescue has struggled through 2022 as Covid lockdowns in China have helped weigh on the price of iron ore and hence FMG although in an even more impressive fashion than BHP, it has been churning out fully franked dividends over recent years. FMG delivered a solid operational update at the end of October despite some obvious cost pressures, and with China now appearing more ‘pro-growth’ we have become interested in direct iron ore exposure having avoided it this year.

- We currently like FMG from both a growth and income perspective, with a preference to buy higher lows than new highs.

MM is bullish FMG around $18.00

Add To Hit List