FMG +4.7% had a good move today after they delivered strong earnings, margin expansion and a dividend ahead of expectations, all underpinned by its industry-leading cost base.

With most operational metrics already flagged at the December quarterly, the headline here was cash generation. Free cash flow more than doubled year-on-year, leverage remained conservative, and the interim dividend came in 24% higher than last year.

1H26 Highlights

- Net income: US$1.91bn, +23% YoY

- Underlying EBITDA: US$4.49bn, +23% YoY (consensus US$3.99bn)

- EBITDA margin: 53% (vs 48% YoY)

- Revenue: US$8.44bn, +10% YoY (beat)

- Iron ore revenue: US$7.53bn, +12% YoY (beat)

- Shipping revenue: US$792m, +1.9% YoY (slightly below)

- Free cash flow: US$1.54bn (vs US$661m YoY)

- Capital expenditure: US$1.67bn, −7% YoY

- Cash on hand: US$4.74bn, +9.6% HoH

- Net debt: US$1.01bn (below estimates)

- Interim dividend: A$0.62, up from A$0.50 (≈65% payout of 1H NPAT)

This was a high-quality, very solid update from Fortescue. They beat on EBITDA, generated cash, held guidance and paid a strong dividend. With costs contained and balance sheet risk low, FMG remains well placed to outperform peers when iron ore sentiment improves.

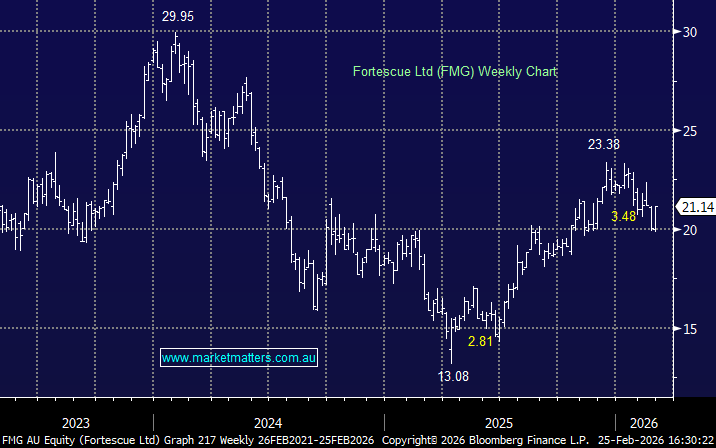

MM remains long & now more bullish on FMG post result

Add To Hit List