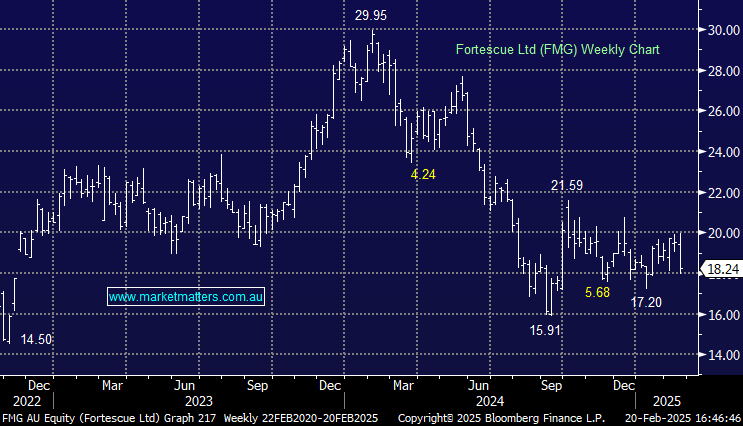

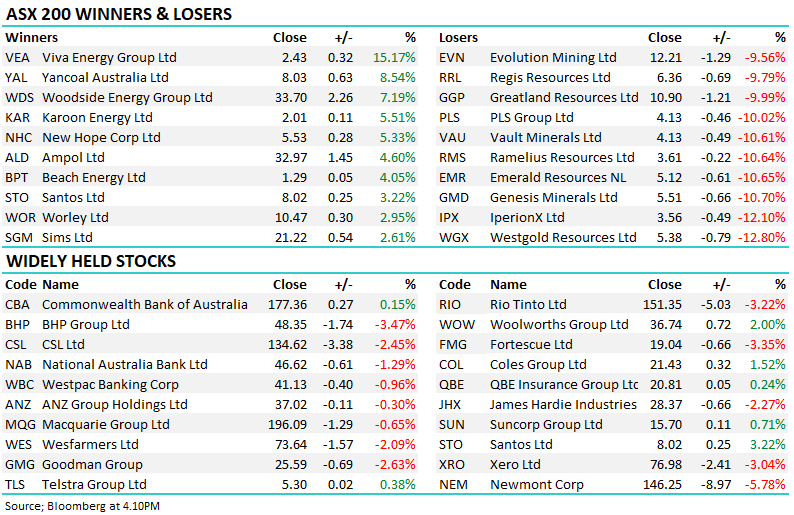

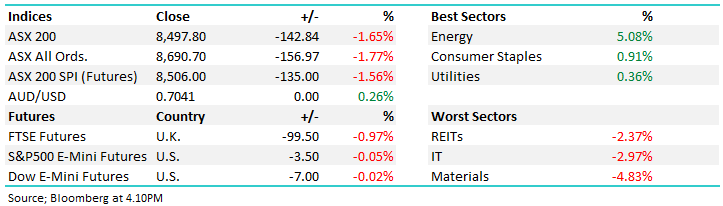

FMG –6.22%: 1H25 result was a slight miss operationally due to higher costs versus consensus and lower revenue. Higher non-cash charges drove a miss on underlying earnings, which translated through to a lower interim dividend.

- Revenue: US$7.64bn vs. consensus US$7.63bn

- Net-profit-after-tax (NPAT) US$1.55bn vs. consensus US$1.76bn

- Capex of US$1.8bn was pre-disclosed, so no surprise there

- Net Debt of US$2.0bn, cash balance sits at US$3.4bn

Looking ahead, FY25 guidance was largely reiterated and capex for the energy division was lowered to US$400m. Decarbonisation efforts remain a focus and are on track to reach real zero emissions by 2030. This will be a headwind from a cost-perspective in the short-term.

While not a great result today, if iron ore prices remain in management’s forecasted range of $80-$100/MT as we think they will, the stock still fits the bill for our Active Income Portfolio paying ~6% fully franked with some growth likely from depressed levels.

MM remains long and cautiously bullish FMG

Add To Hit List