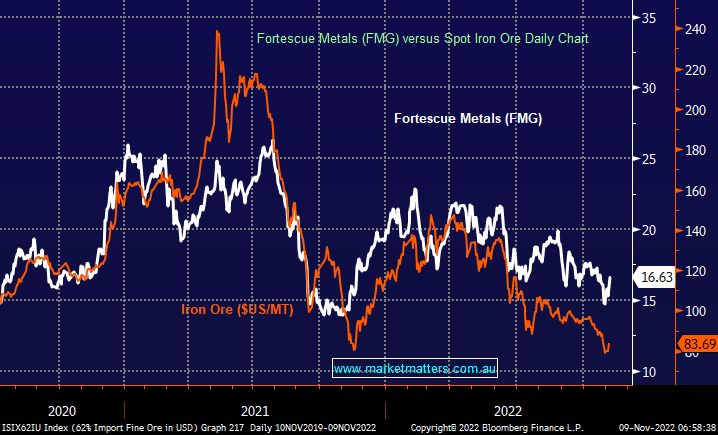

At the end of October, Fortescue reported a good operational update with solid production setting up the company for another record year, however, two headwinds were obvious and these need to ease for the FMG share price to rally. Iron Ore prices have been weak as Chinese lockdowns continue, reducing the demand for Iron Ore with prices last week hitting ~US78/tonne down from $US160/tonne in April, while cost pressures are also obvious throughout their operations – costs up 16% YoY thanks to higher expenditure on diesel and labour. There are always headwinds to discuss when share prices are near 52-week lows and FMG is no exception, however, what comes next is important. Many higher-cost Iron Ore producers are losing money at current prices which is unsustainable over longer periods of time, while Chinese lockdowns will end (at some point). As the $US eases & China moves closer to re-opening and some stimulus to boost tepid growth, Iron Ore is starting to look interesting again.

- On consensus expectations, FMG is expected to yield 9.47% in FY23, dropping to 6.85% in FY24.

MM is now bullish on FMG ~$16.50 for Income & Growth

Add To Hit List