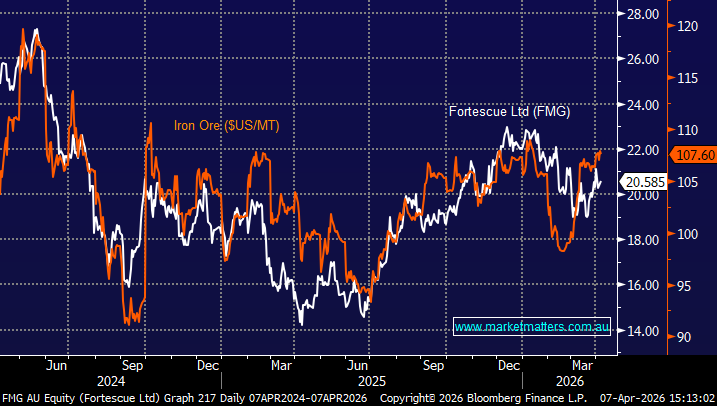

As we mentioned we hold BHP in our Active Income Portfolio with the iron ore exposure supported by pure play FMG, i.e. currently 12% of our income portfolio has iron ore exposure. This is a simpler story than BHP and Rio, with FMG offering direct leverage to iron ore. As the chart below illustrates, if prices hold above ~$US100, the stock should benefit, supported by an attractive ~6% fully franked yield.

- We remain constructive on iron ore, and with FMG offering a strong yield, we see it as a compelling story for income

Fortescue rallied following its strong February result, delivering solid earnings, expanding margins (~53%) and a better-than-expected dividend, underpinned by its industry-leading cost base. The standout was cash generation, with free cash flow more than doubling year-on-year and the balance sheet remaining conservatively geared, positioning FMG well to outperform if iron ore sentiment improves.

- If/when iron ore does advance towards our target MM is likely to reduce our exposure to the bulk commodity in this portfolio.

chart

Fortescue Group (FMG) v Iron Ore ($US/MT)

chart

Fortescue Group (FMG) v Iron Ore ($US/MT)

If our view on both the ASX and iron ore proves correct, FMG looks attractive from a risk/reward perspective, following its recent ~21% pullback, supported by an anticipated ~70c fully franked dividend in August.

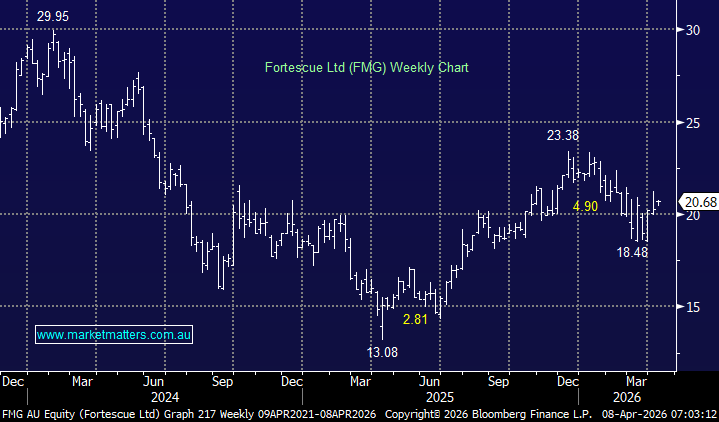

- We are targeting a test of the $23.50-24 area through 2026.

MM is bullish towards FMG around $20.70

Add To Hit List