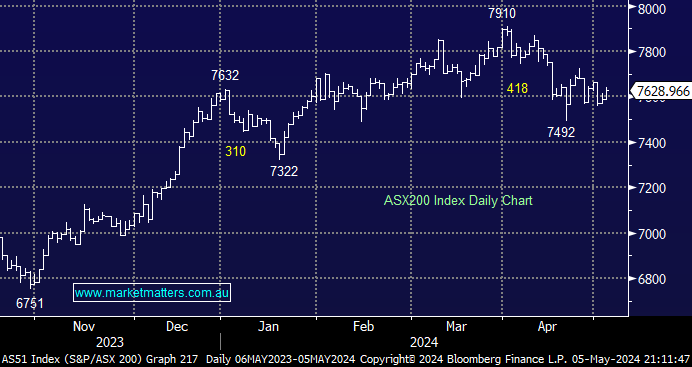

The ASX200 rallied +0.7% higher last week as easing bond concerns saw the rate-sensitive stocks/sectors recover strongly, e.g. The Real Estate +3.2%, Tech +2.3%, and Consumer Discretionary +2.1% sectors rallied. After Friday’s market friendly employment data, we expect more of the same at the start of the second week of May, aided by a more than 3% surge by US Tech following Apple’s (AAPL US) earnings beat – the US$2.8 trillion-dollar stock surged almost 6%.

- The SPI Futures are pointing to a +0.3% advance this morning after broad-based gains in the US on Friday night – BHP closed up 10c in the US.

MM remains cautiously bullish toward the ASX200 around the 7600 area

Add To Hit List

US equities enjoyed easing bond worries last week, plus a solid earnings period to date, which so far has seen 77% of companies beat at the EPS line, with around 80% of the S&P500 having reported. During the past week, positive earnings surprises were reported by companies in a number of sectors, led by the healthcare and consumer discretionary, although positive quarterly earnings from Amazon and Apple dominated the headlines.

- The US NASDAQ has corrected ~8% over recent weeks from its March all-time high; a push higher towards 19,000 wouldn’t surprise from here.

MM remains bullish towards US stocks in the medium term

Add To Hit List

The UK FTSE again posted new all-time highs on Friday night, with tech and retail stocks leading the charge as bond fears dissipated following the market-friendly US employment data. Hiring slowed sharply in April, and wage growth eased without signalling a serious deterioration in the jobs market.

- No change; We remain bullish towards the UK FTSE, a positive read-through on the highly correlated ASX, especially the miners.

MM remains bullish towards the UK FTSE medium-term

Add To Hit List