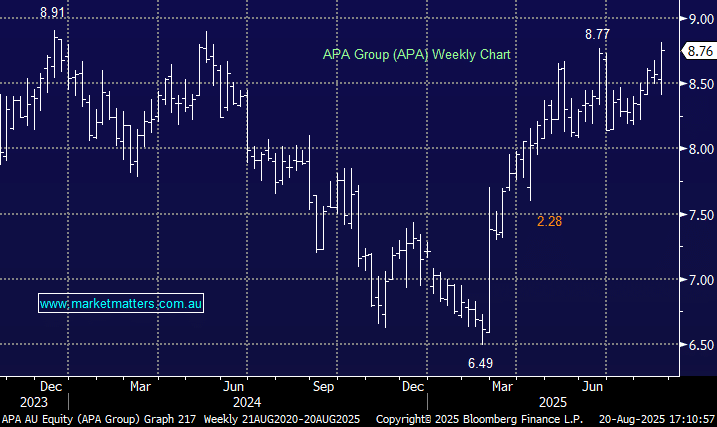

APA +3.42%: Released a solid FY25 result with earnings at the top of guidance and marginally above consensus. We hold this utility in both our income and growth portfolios.

- Revenue of $3.20bn was up 4.6% y/y

- Earnings before interest tax depreciation amortization (EBITDA) of $1.89 billion +9.1% y/y.

- NPAT of $129mn was down 87% y/y.

- Full-year dividend totalled 57c up from 56c a year prior.

EBITDA guidance of $2.12–2.20 billion was in line with estimates and a forecast dividend of $0.58 is solid given expansion capex upgraded from $1.8 to $2.1 billion over the next 3 years. This is the sort of solid result you want from a high-yielding defensive utility.

MM is bullish towards APA

Add To Hit List