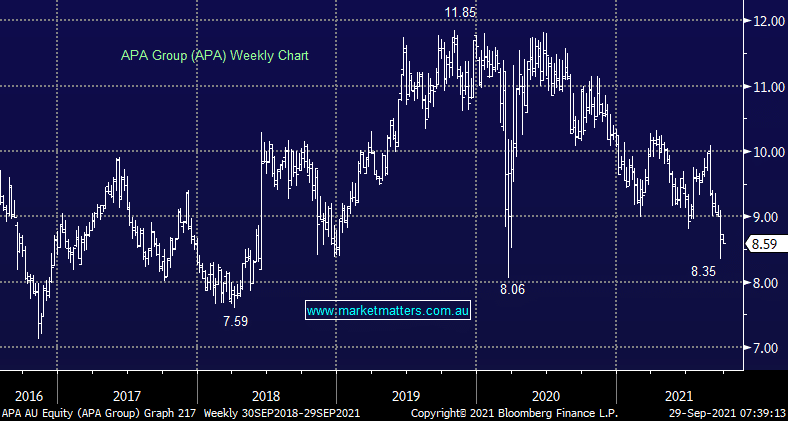

APA Group is one of Australia’s largest energy infrastructure businesses with ~$20b worth of assets around the country that include gas pipelines as well as other transmission assets. As the energy mix changes more towards renewables, transmission of energy will remain key and APA is very well positioned here against a backdrop of rising foreign interest & ownership. The sell-off in the APA stock price recently is for 3 key reasons:

- They are in the running to buy Basslink, an electricity interconnector that allows the trade of electricity between Tasmania & the National Electricity Market. They would need to raise capital to do this.

- They have also made a play for electricity poles and wires business AusNet Services (AST) trumping an existing offer from Canadian based Brookfield. They would need to raise ~$1.5bn in equity if successful here.

- Rising bond yields are a negative for long life infrastructure assets – they are bond like in their return profile

While these are negatives for the share price short term, we think the purchases outlined above make sense and any new equity would be issued on the pro-rata basis, i.e. based on current shareholdings as Transurban (TCL) has done. On a call this week, they stressed that AusNet was their main priority and Basslink would be nice but not critical. APA offers a defensive earnings stream and a ~6% unfranked yield.

MM is now bullish APA as a defensive income play

Add To Hit List