Fortescue rallied after delivering a high-quality result in February, with strong earnings, expanding margins and a dividend ahead of expectations, all underpinned by its industry-leading cost base. While most operational metrics were already flagged, the key standout was cash generation, with free cash flow more than doubling year-on-year and the balance sheet remaining conservatively geared. Earnings beat expectations, margins lifted to 53%, and the interim dividend rose 24% to $0.62. With costs well contained, solid cash generation and low leverage, FMG is well positioned to outperform peers as iron ore sentiment improves.

This is a simpler beast than BHP and RIO. If iron ore remains above $US100, the stock should appreciate, aided by its forecast ~6% fully franked yield.

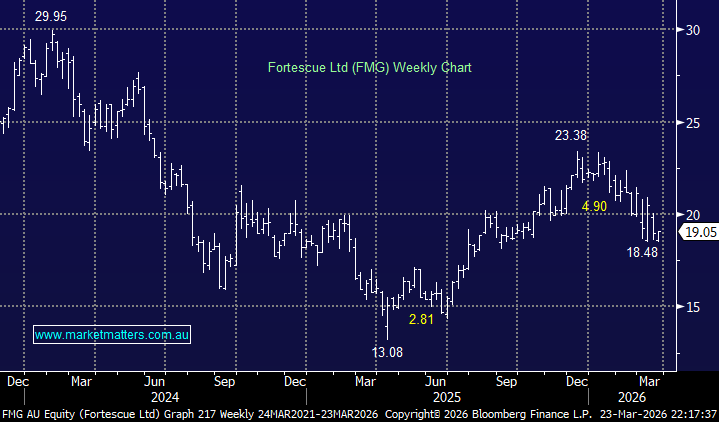

- We can see FMG testing $25 in the coming year, assuming MM is correct toward iron ore – MM owns FMG in its Active Income Portfolio.

MM is long and bullish toward FMG around $19

Add To Hit List