Slightly soft financial metrics for the first-half relative to consensus, but a big uplift in earnings YoY underpinned by stronger copper prices, higher volumes and improved operating leverage across its core assets.

- Underlying earnings: $107.1m (vs $49.1m last year) – consensus $108m

- Underlying EBITDA: $304.5m (+19% y/y) – consensus $308m

- Sales revenue: $672.1m (+17% y/y) – consensus $678.7m

- Interim dividend: Nil (unchanged)

Earnings pretty much doubled for SFR while revenue narrowly missed consensus, margins and cost control remained well aligned with guidance. They increased FY capex guidance to $240m (from $230m), reflecting increased activity at the Kalkaroo project as it ramps through the second half. Importantly, Sandfire retained all production and cost guidance across MATSA and Motheo, with volumes weighted to 2H. Copper equivalent production of 72.1kt in 1H leaves the group well positioned to hit full-year targets, while balance sheet flexibility remains intact despite higher investment spend.

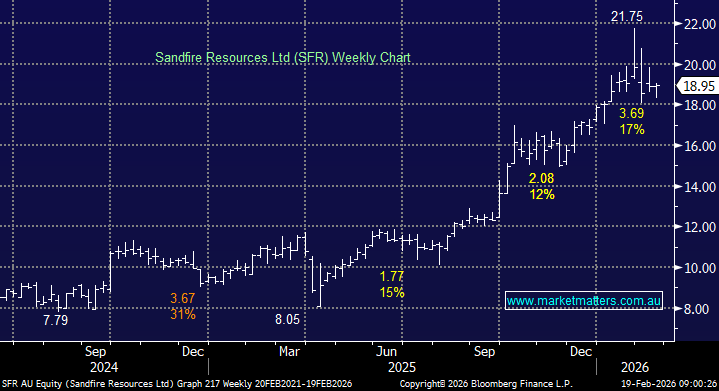

MM remains long & bullish SFR

Add To Hit List