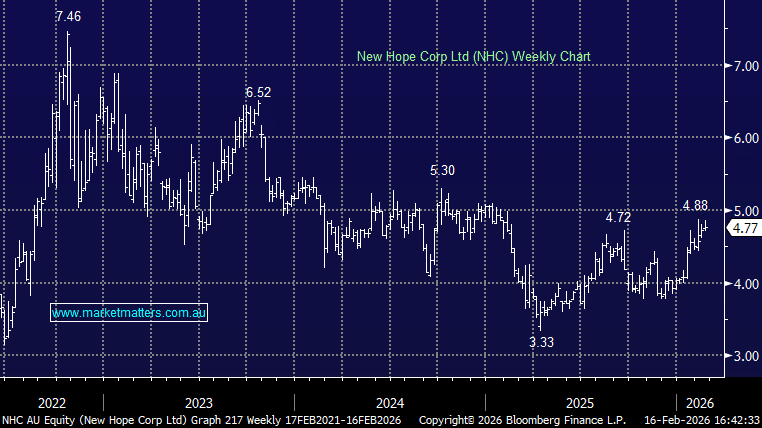

NHC +1.06%: Reported a steady December-quarter operational update, with improving volumes and reaffirmed FY26 guidance.

- ROM coal production 4.06mt, +4.8% QoQ

- Coal sales volumes 2.90mt, +8.2% QoQ

- 1H underlying EBITDA $214.8mn

The key positive was Bengalla, where sustaining capex guidance was trimmed to $100–130mn (from $130–160mn) as pit sequencing returns to normal, a clear positive for cash generation.

Overall, a no-surprises update with volumes moving in the right direction, guidance reaffirmed, and a capex guidance downgrade. In a supportive coal price environment, NHC offers robust cash generation to fuel capital returns – that fits the bill to continue holding the stock in the Active Income Portfolio.

MM remains long and bullish NHC ~$4.80

Add To Hit List