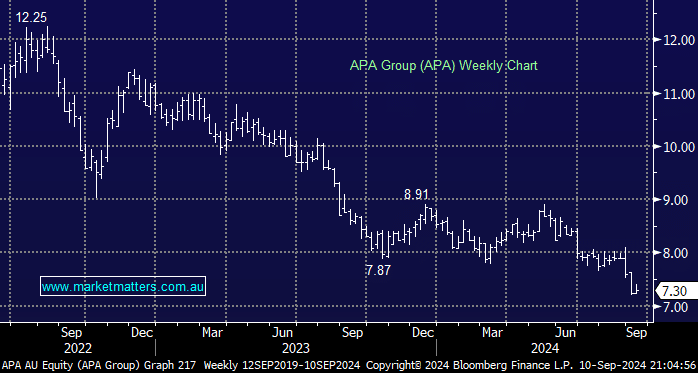

APA Group is the largest owner of natural gas transmission infrastructure in Australia and has been under significant pressure, with the share price down nearly 15% in the past year to a recent low of ~$7.20. This has prompted an increase of inbound enquiries on what we intend to do with our position held in the Income Portfolio; having purchased at $9.82 in May of 2023, the position is currently down ~16% inclusive of accrued dividends. This was our 2nd tilt at APA in recent years, having originally sold out ~$12 in July of 2022, booking a healthy 45% profit, a significant return on what is a very stable business.

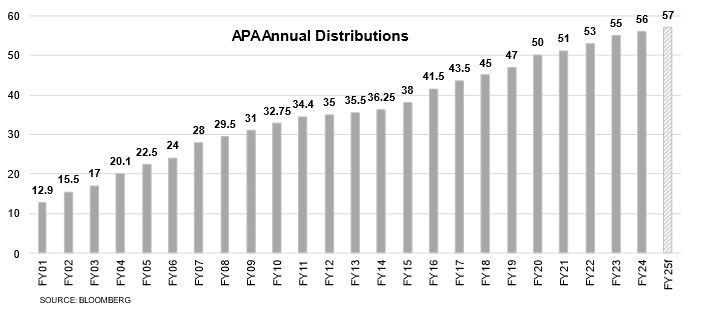

There are reasons for its recent weakness, including higher costs, regulatory scrutiny on one of its assets, higher bond yields and some uncertainty around future investment, however, if we stand back and simply acknowledge the dividends APA has paid since 2001, it should provide some confidence for what comes next. For the past 23 years, APA has grown distributions every year, as the below chart shows, and now trades on a guided yield (from the company) of 7.7%, which is extremely attractive for income-focused portfolios.

chart

APA Annual Distributions – Source Bloomberg

chart

APA Annual Distributions – Source Bloomberg

Relative to 10-year US bond yields at 3.7%, the spread has blown out to 400bps compared to its historical spread of 280bps over bonds, and a low of 200bps when we sold out of our last position back in 2022. The spread should be thought of as the ‘risk premium’ or compensation over and above a risk-free asset. For instance, a typical major bank hybrid with 5-years to first call now trades at ~200bps over bank bills, a 10-year bond in QANTAS launched yesterday was priced at 210bps over, and with APA we now have a regulated utility, with regulated cash flows i.e.very bond like in nature, trading with a 4% risk margin over bonds.

- We remain very confident in our position in APA Group and would flag it as a top-income investment at current levels.

MM remains long & bullish APA for income.

Add To Hit List