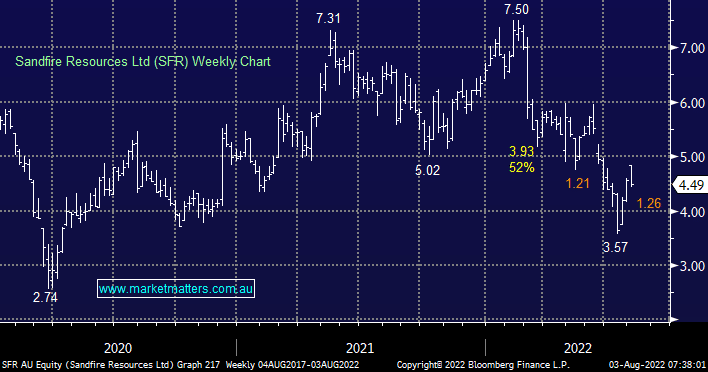

The emerging copper producer presented at the Diggers & Dealers conference yesterday. FY22 was a big year for the company, buying the MATSA copper operations in Spain to go with their WA asset DeGrussa. They are also less than 12 months from production at Motheo in West Africa to further expand their production profile. Weaker copper prices and global growth fears have clearly weighed on shares while energy costs were also climbing, particularly impacting the MATSA operation, however operationally, SFR are starting to deliver after many tough years.

In MM’s view, there is still plenty of value to be added from this operation though, with further resource upgrades and better utilisation, costs will likely ease in the long run. Sandfire now also have a number of growth options as well with Motheo coming online and the potential to expand operations in WA. The outlook for the copper market is important, and we are bullish here in the medium term, while SFR is also a bit of a ‘self-help’ story.

MM is bullish SFR around $4.50

Add To Hit List