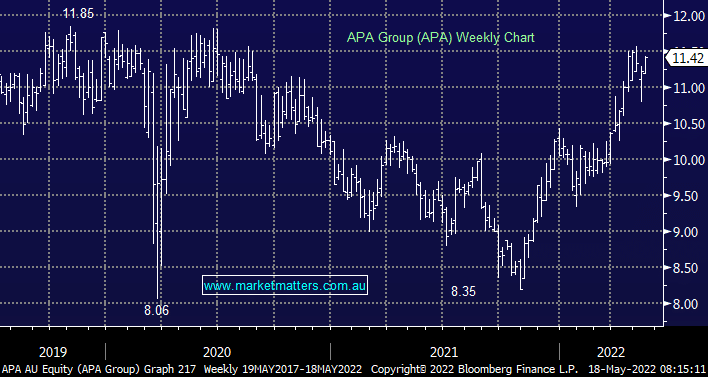

APA has been a solid performer in the Income Portfolio sitting on a paper profit of ~35%, which for a regulated utility involved in gas pipelines where revenue growth is set at low levels is a good outcome, however, we ask ourselves what is going to drive appreciation from here?

At a recent strategy day, APA did a good job of trying to broaden the market’s perception of them away from being purely gas pipelines and more towards energy infrastructure which includes involvement in the electrification of the grid. In short, they believe that any smooth transition to renewables will need more gas while they also want to be involved in renewables themselves such as batteries & other renewable assets, and they articulated a strong business case for this.

The other obvious aspect to consider for APA and other infrastructure stocks is debt in a rising interest rate environment, however in APA’s case, 99% of their contracted revenue is linked to CPI (inflation), 30% of it is actually linked to US CPI which is running hotter than our own. While APA is not cheap after its solid run in price, we still view an expected yield of 4.7% (unfranked) with upside potential as attractive, particularly given how scarce quality infrastructure assets are on the ASX.

MM remains neutral/bullish APA

Add To Hit List