The ASX200 slipped -0.36% on Tuesday, but the pronounced stock/sector rotation is what caught our attention. The stimulatory rhetoric out of Beijing on Tuesday saw aggressive buying return to the ASX miners, in a similar fashion to late September.

The ASX200 staged an impressive recovery on Monday after being down ~50 points at around 11 am; 8 of the main board's 11 sectors closed higher which was enough to see the index eke out a small gain for a day that saw an absence of selling into early weakness.

Momentum mania is sweeping both Wall Street and the ASX, with the risk party continuing unabated on Friday night. The S&P 500 ended last week at fresh records, helped by a +28% gain by the NASDAQ this year.

The ASX200 closed up +0.15% on Thursday in an ultimately lacklustre session, which promised more in the morning before surrendering two-thirds of its gains through the afternoon. Tech and consumer discretionary names advanced over 1% while real estate lagged, slipping -1.4%. On the commodities front, the story remains the same, and it’s starting to get a little bit monotonous as we head into Christmas, less than three weeks away.

After yesterday's close, China Investment Corporation (CIC) launched a massive $1.9 billion selldown of market darling Goodman Group (GMG). Citi’s equities desk was looking to place 50.4 million GMG shares or about 2.6% of the company; to put things into perspective, only 3.7 million shares exchanged hands on Tuesday.

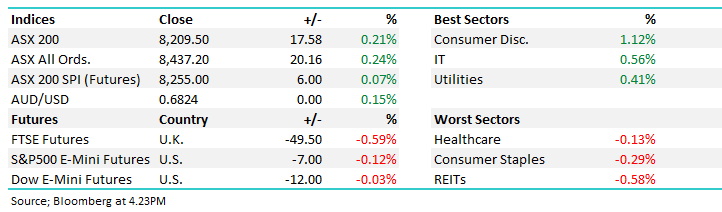

The ASX200 closed up +0.1% on Monday in a fairly lacklustre session, which again saw the local index unable to build on early gains. Over 50% of the main board closed higher, with interesting moves in the resources sector after Chinese manufacturing data beat estimates.

The ASX200 is set to test new highs early this week after US equities hit new milestones on Friday, even though it was only a half-day following Thanksgiving holiday. The path of least resistance remains on the upside, even on quiet days.

The ASX200 closed up +0.45% on Thursday, but again, after nudging a fresh all-time high, it drifted lower into the close, this time surrendering almost half of its late afternoon gains. The advance was patchy, with over 40% of the main board closing lower, but when the “Big Four Banks,” BHP, and CSL all rally, it's going to be a tough session for the bears.

The ASX200 rebounded +0.6% on Wednesday, retracing more than 50% of Tuesday's sell-off following Trump’s tariff threats, although we believe he simply reiterated his campaigning rhetoric. Gains were broad-based in the session, with all 11 sectors finishing higher and over 65% of the main board rose.

The ASX200 staged an impressive recovery on Monday after being down ~50 points at around 11 am; 8 of the main board's 11 sectors closed higher which was enough to see the index eke out a small gain for a day that saw an absence of selling into early weakness.

Momentum mania is sweeping both Wall Street and the ASX, with the risk party continuing unabated on Friday night. The S&P 500 ended last week at fresh records, helped by a +28% gain by the NASDAQ this year.

The ASX200 closed up +0.15% on Thursday in an ultimately lacklustre session, which promised more in the morning before surrendering two-thirds of its gains through the afternoon. Tech and consumer discretionary names advanced over 1% while real estate lagged, slipping -1.4%. On the commodities front, the story remains the same, and it’s starting to get a little bit monotonous as we head into Christmas, less than three weeks away.

After yesterday's close, China Investment Corporation (CIC) launched a massive $1.9 billion selldown of market darling Goodman Group (GMG). Citi’s equities desk was looking to place 50.4 million GMG shares or about 2.6% of the company; to put things into perspective, only 3.7 million shares exchanged hands on Tuesday.

The ASX200 closed up +0.1% on Monday in a fairly lacklustre session, which again saw the local index unable to build on early gains. Over 50% of the main board closed higher, with interesting moves in the resources sector after Chinese manufacturing data beat estimates.

The ASX200 is set to test new highs early this week after US equities hit new milestones on Friday, even though it was only a half-day following Thanksgiving holiday. The path of least resistance remains on the upside, even on quiet days.

The ASX200 closed up +0.45% on Thursday, but again, after nudging a fresh all-time high, it drifted lower into the close, this time surrendering almost half of its late afternoon gains. The advance was patchy, with over 40% of the main board closing lower, but when the “Big Four Banks,” BHP, and CSL all rally, it's going to be a tough session for the bears.

The ASX200 rebounded +0.6% on Wednesday, retracing more than 50% of Tuesday's sell-off following Trump’s tariff threats, although we believe he simply reiterated his campaigning rhetoric. Gains were broad-based in the session, with all 11 sectors finishing higher and over 65% of the main board rose.

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

Verication email sent.

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

!

Invalid One Time Password

Please check you entered the correct info, please also note there is a 10minute time limit on the One Time Passcode

To reset your password, enter your email address

A link to create a new password will be sent to the email address you have registered to your account.

Market Matters members receive daily market reports, real-time trade alerts, full access to 5 portfolios and dynamic company data.

Choose how you'd like to proceed:

We have a range of membership options to suit your needs and budget, why not join today and get unlimited access to the premium Market Matters service.