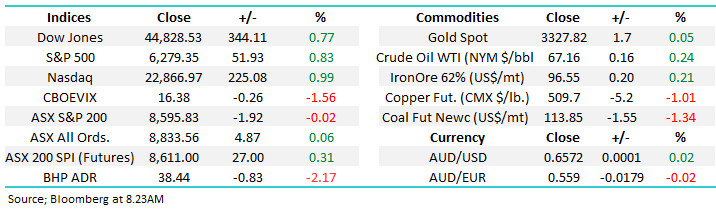

The ASX200 enjoyed an explosive start to the week with over 80% of the main board advancing led by the banks, energy and tech stocks, if we take the gold sector out of the mix it was almost a clean sweep for the bulls. There are only 3 trading days left of this financial year hence the easiest call for the next few sessions is we should expect plenty of volatility under the hood of the market, in both directions. Second-guessing which stocks will surge or plunge is akin to a game of two-up hence we would rather step back and see if anything becomes too cheap or expensive and then we can act accordingly i.e. don’t be surprised if you receive another trading alert over the coming week.