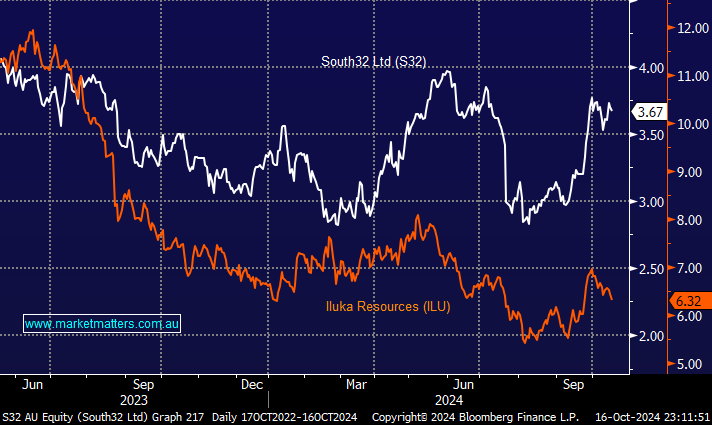

We are long S32 in our Active Growth Portfolio, a position that has benefitted nicely from stimulatory moves out of Beijing and simply buying at depressed levels – year-to-date, the stock has advanced over 10%. Conversely, Iluka (ILU) is down over 4% as the traditional mineral sands operator branches out into rare earths. South32 hasn’t got our favourite commodity mix out of the ASX miners, especially with its high levels of revenue coming from aluminium/alumina; if Trump and Putin rekindle their friendship, increased supply could hit the market. At this stage of the cycle, ILU is highly correlated to the ESG names, which we see lower in the short-term. However, we will be watching the S32 – ILU stretching elastic band over the coming months.

- We like ILU as an excellent proxy for exposure to a turnaround in the Chinese property market. This crisis has weighed on ILU, which has halved from its 2023 high.

MM likes both ILU and S32 into 2024

Add To Hit List